Every prediction market trade — whether you’re buying a Fed rate contract on Kalshi or a Super Bowl position on Polymarket — runs through an order book. The order book determines what price you pay, how fast your trade executes, and whether you’re charged a maker or taker fee.

If you’ve read our prediction market fees breakdown, you already know that maker and taker fees vary dramatically across platforms. This page explains the mechanics underneath: what the order book actually is, how different order types interact with it, and why it matters for the price you get.

Most prediction market explainers stop at “buy yes, buy no, $1 payout.” We’re going deeper. If you already understand how event contracts work, this is the next layer.

What the order book is

A prediction market is not a sportsbook. There’s no house. No one is setting odds and taking the other side of your bet. Prediction markets are peer-to-peer exchanges — every yes buyer is matched with either a no buyer or a yes seller. The platform facilitates the match. It doesn’t take the position.

The order book is the mechanism that makes this matching work. It’s a live, continuously updated list of every open buy and sell order for a given contract.

When you pull up a market like “Will the Fed cut rates in March?”, the order book shows you two things: the prices at which other traders are willing to buy (bids), and the prices at which other traders are willing to sell (asks). The number of contracts available at each price is also visible.

Both Kalshi and Polymarket use what’s called a central limit order book, or CLOB. Same structure as the NYSE and Nasdaq — all orders for a given contract are collected in one place, and the system matches buyers with sellers according to a transparent set of rules. Prediction markets didn’t invent a new matching engine. They borrowed one that already worked.

The difference is scale. A stock like Apple trades in a single, massive liquidity pool. A prediction market contract like “Will Bitcoin close above $100K on March 31?” is its own isolated order book with its own set of buyers and sellers. Every new question creates a new book, and every new book starts from zero.

This is why liquidity is one of the most important concepts in prediction markets, and one we cover in detail in our liquidity guide. It’s as if the NYSE had to build a brand new trading floor every time someone asked a question about the weather.

Bids, asks, and the spread

When you look at an order book, you see three things that tell you almost everything you need to know about a market’s trading conditions.

- Bids are buy orders. They represent what traders are willing to pay for a contract right now. The highest bid is the best price any buyer is currently offering. If the highest bid on a yes contract is 62¢, that means someone has an open order to buy at 62¢ — and no one is willing to pay more than that at this moment.

- Asks are sell orders. They represent the prices at which traders are willing to sell. The lowest ask is the cheapest price at which you can buy a contract immediately. If the lowest ask is 65¢, you can buy right now — but you’re paying 65¢, not the 62¢ bid.

- The spread is the gap between the highest bid and the lowest ask. In the example above, the spread is 3¢. That 3¢ is the cost of immediacy — the premium you pay for executing right now instead of placing a limit order and waiting.

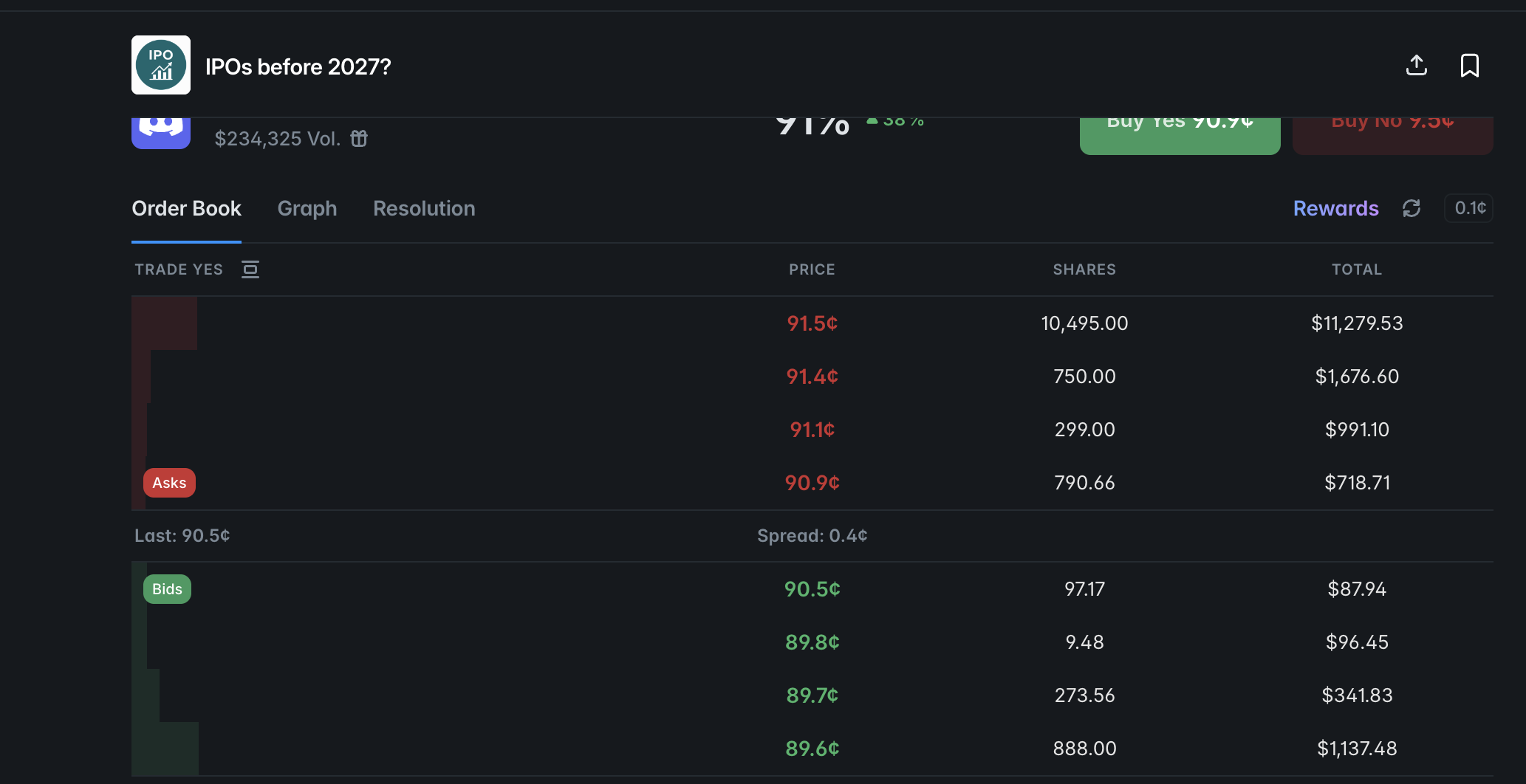

Tight spreads (1–2¢) mean the market is liquid and well-traded. Wide spreads (5¢ or more) signal thin liquidity, uncertainty, or both. For context, the Discord IPO market on Polymarket currently shows a 0.4¢ spread — about as tight as you’ll see on any prediction market.

One detail that trips up traders coming from sportsbooks: in prediction markets, yes and no prices always add up to roughly $1.00. If yes costs 62¢, no costs 38¢. That’s because every trade has two sides — someone buying yes is always matched with someone buying no. The prices reflect how likely traders think the outcome is.

You can see this on the “IPOs before 2027?” market — Discord shows “Buy Yes 90.9¢” and “Buy No 9.5¢” side by side. Those two prices add up to just over $1.00. Buying no at 9.5¢ is the same as selling yes at 90.5¢.

Some platforms display separate tabs for yes and no, which can look like two independent order books. They’re not. It’s one book — the yes side and the no side are just two ways of looking at the same set of orders. On Polymarket especially, the tab layout can make this confusing. Just remember: yes price + no price ≈ $1.00, always.

The spread also tells you something about information quality. If a market is priced at 50¢ but the spread is 10¢, that means the best bid is 45¢ and the best ask is 55¢. The “50%” implied probability is really “somewhere between 45% and 55%.” The wider the spread, the less precise the market’s signal.

Market orders vs. limit orders

Every prediction market gives you two ways to trade: market orders and limit orders. Which one you choose determines your execution speed, your price, and your fees.

Market orders execute immediately at the best available price. You’re “taking” liquidity off the book — matching against someone else’s resting order. On Kalshi, these are labeled “quick orders.” The advantage is speed. You get your position instantly.

The disadvantage is price uncertainty. If the best ask is 65¢ with only 100 contracts available and you want 500 contracts, your order eats through multiple price levels. You might fill 100 at 65¢, 150 at 66¢, and 250 at 67¢. Your average fill is 66.3¢, not the 65¢ you saw on screen.

Market orders typically incur taker fees — on Kalshi, that’s the higher of its two fee tiers, and on Polymarket, taker fees apply on eligible markets including 15-minute crypto, 5-minute crypto, NCAAB, and Serie A contracts.

Limit orders let you set your own price. Your order sits on the book and waits for someone to trade against it. You’re “making” liquidity — adding depth that other traders can execute against.

On Kalshi, limit orders come with expiration options: IOC (immediate-or-cancel, meaning your order either fills right now at your price or gets cancelled entirely — nothing sits on the book), EOD (the order stays active until end of day), or a custom expiration you set. On Polymarket, limit orders rest on the book until filled or cancelled.

The fee advantage is significant. Polymarket charges 0% for maker orders and redistributes taker fees daily to liquidity providers through its Maker Rebates Program.

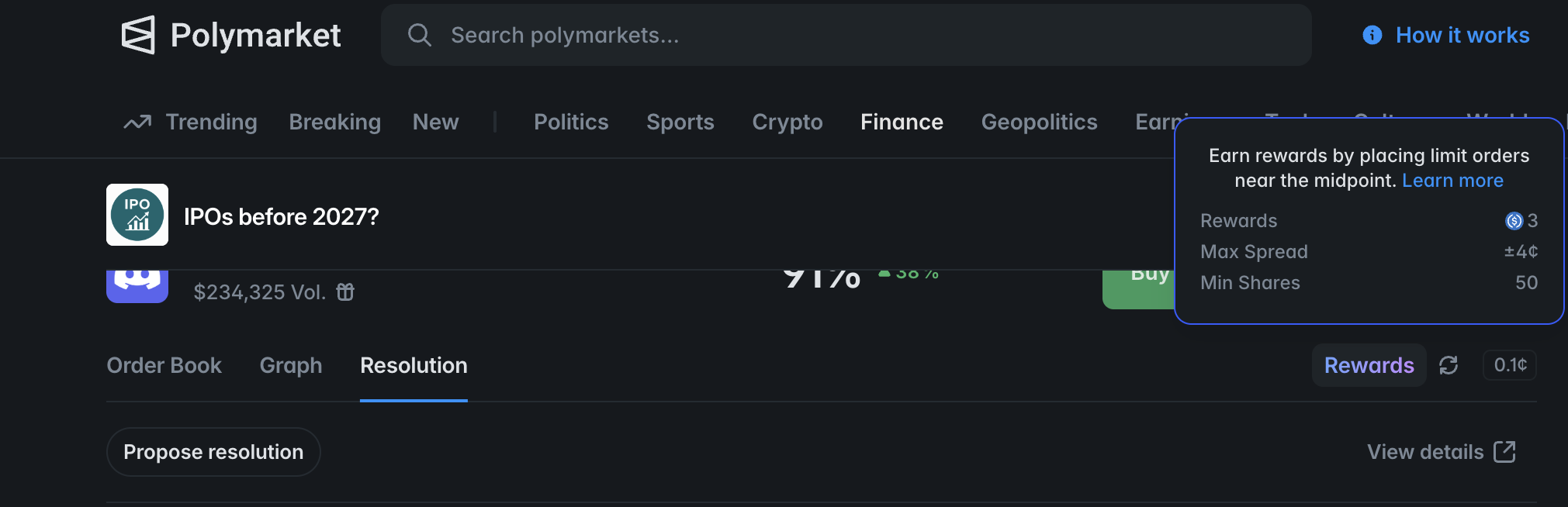

It also runs a separate liquidity rewards program — on the Discord IPO market, for example, Polymarket offers rewards to anyone placing limit orders within ±4¢ of the midpoint with a minimum of 50 shares. You’re literally getting paid to add depth to the book.

On Kalshi, makers pay reduced fees and receive rebates on select high-volume markets. Placing a limit order means you control your entry price, avoid slippage, and pay less to trade. In most of life, the patient option and the cheap option are different things. On a prediction market order book, they’re the same thing.

The tradeoff is time. A limit order at 62¢ only fills if the market moves to your price. If it never gets there, you don’t trade. Sometimes that’s fine. In fast-moving markets — a breaking news event, a last-second line shift — it’s not. The certainty of a market order can be worth the extra cost.

How orders match

When your order enters the book, it follows a simple set of rules called price-time priority. This is the same matching logic used by every major stock exchange.

- Price priority means better-priced orders fill first. Two traders have buy orders on the book — one at 66¢, one at 65¢. A seller comes in at 65¢. The 66¢ buyer gets filled first. Better price, first in line.

- Time priority breaks ties. If two traders both have buy orders at 65¢, the one who placed their order first gets filled first. First in, first out.

- Partial fills happen when there aren’t enough contracts at your target price to complete your full order. If you want 500 contracts at 62¢ but only 200 are available, you get 200 filled. The remaining 300 either sit on the book waiting for more sellers (if you placed a limit order) or get cancelled (if you placed an IOC order on Kalshi). On a market order, the remaining contracts fill at the next available price level — which is where slippage comes from.

These rules are transparent and mechanical. There’s no discretion, no preferential treatment, no hidden queue. Every trader sees the same book and follows the same matching logic. Nobody’s going to limit your account for winning too much. The matching engine doesn’t know or care who you are.

Reading market depth

The price displayed on a market card — “Yes: 65¢” — is usually the last traded price or the midpoint between the best bid and ask. It tells you what happened on the last trade. Not what will happen on yours. For anything beyond a small order, you need to look at depth.

Depth is the number of contracts available at each price level in the order book. A market with 5,000 contracts at the best ask is deep — your order fills without moving the price. A market with 50 contracts at the best ask is thin — even a modest order pushes you into worse price levels.

Here’s what this looks like on an actual market. At the time of writing, Polymarket’s “IPOs before 2027?” market has a Discord outcome trading at 91% with $234,325 in volume. The yes-side order book looks like this:

Asks (what you pay to buy yes):

- 790 shares at 90.9¢ ($718 total)

- 299 shares at 91.1¢ ($990 total)

- 750 shares at 91.4¢ ($1,676 total)

- 10,495 shares at 91.5¢ ($11,279 total)

Bids (what you get if you sell yes):

- 97 shares at 90.5¢ ($87 total)

- 9 shares at 89.8¢ ($96 total)

- 273 shares at 89.7¢ ($341 total)

- 888 shares at 89.6¢ ($1,137 total)

The spread is 0.4¢ — tight for a contract priced this high. But look at the depth asymmetry. On the ask side, there are nearly 800 shares available at the best price. You could spend about $718 and fill cleanly at 90.9¢. On the bid side, there are only 97 shares at the best price.

If you tried to sell 500 shares, you’d blow through the 90.5¢ level, the 89.8¢ level, and land somewhere around 89.7¢. Your average fill would be roughly 89.8¢ — about 0.7¢ worse than the displayed bid. The order book doesn’t care what price you saw on the card. It cares what’s actually on the shelf.

That asymmetry — deep asks, thin bids — tells you something. Market makers are comfortable offering shares near 91¢, but there are far fewer buyers placing open orders on the bid side. If you wanted to exit a large yes position in a hurry, you’d pay for it.

This is why depth matters more than the displayed price. On high-volume markets — major elections, Fed meetings, NFL championship games — order books are typically deep enough that a $10,000 position fills without significant price movement.

On Polymarket, flagship markets can absorb $50,000 to $100,000+ in order flow with minimal slippage. On Kalshi, high-volume markets generally support trades up to around $10,000 before slippage becomes noticeable.

But the majority of prediction markets don’t operate at those levels. According to analysis from BlockBeats, most markets on both Kalshi and Polymarket have total trading volume below $10,000. On those markets, a single large position can cause double-digit percentage price swings.

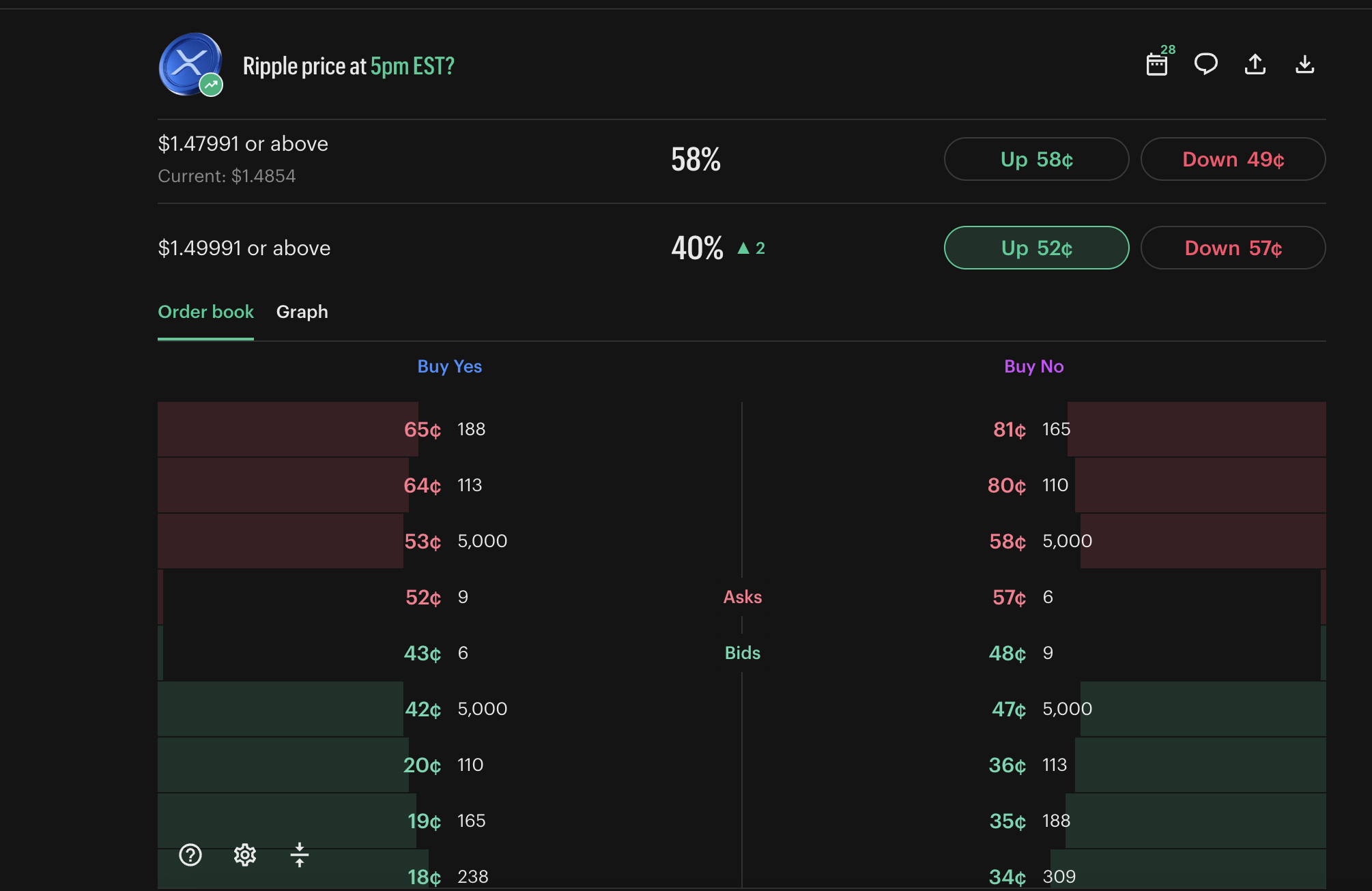

Now compare that to a 15-minute Ripple price contract on Kalshi. The spread is 9¢ — over 20 times wider than the Discord book. At the best ask, there are 9 contracts available. At the best bid, 6. Below that, the book jumps straight to a wall of 5,000 contracts at 53¢ and 42¢, with almost nothing in between.

This is what a thin book looks like in practice. The 5,000-contract walls are likely resting market maker orders — they’ll provide a floor and ceiling, but they’re far from the current price. If you wanted to buy 15 contracts, you’d fill 9 at 52¢ and 6 at 53¢. Your average cost: roughly 52.4¢. Not terrible — but only because the 5,000-contract wall at 53¢ absorbed the overflow. Beyond that wall, the next price level is 64¢. That’s an 11¢ gap with almost nothing in between.

Think of it like a vending machine with one bag of chips on the front row and the rest of the stock pushed to the back. The price on the label says $2. You’ll get one bag for $2. But if you want five, someone has to go to the stockroom, and the price just went up.

On any market outside the top-tier flagship events, check the order book before you trade. If you don’t, the price you see on the card and the price you actually pay could be cents apart.

How Kalshi and Polymarket order books differ

Both platforms use central limit order books, but the underlying architecture is different in ways that affect how your orders execute and settle.

Kalshi runs a fully centralized central limit order book (CLOB). All order matching happens on Kalshi’s servers, and the entire trading infrastructure operates within its CFTC-regulated framework as a Designated Contract Market (DCM). You place an order, it matches on Kalshi’s engine, and the trade settles within Kalshi’s system.

Order types include quick orders (market orders that fill immediately) and limit orders with IOC, EOD, or custom expiration. Kalshi differentiates between makers and takers in its fee schedule — makers pay reduced fees, and on select markets, Kalshi offers maker rebates. The Robinhood integration means that Kalshi’s order book also receives flow from Robinhood’s Prediction Markets, adding retail depth.

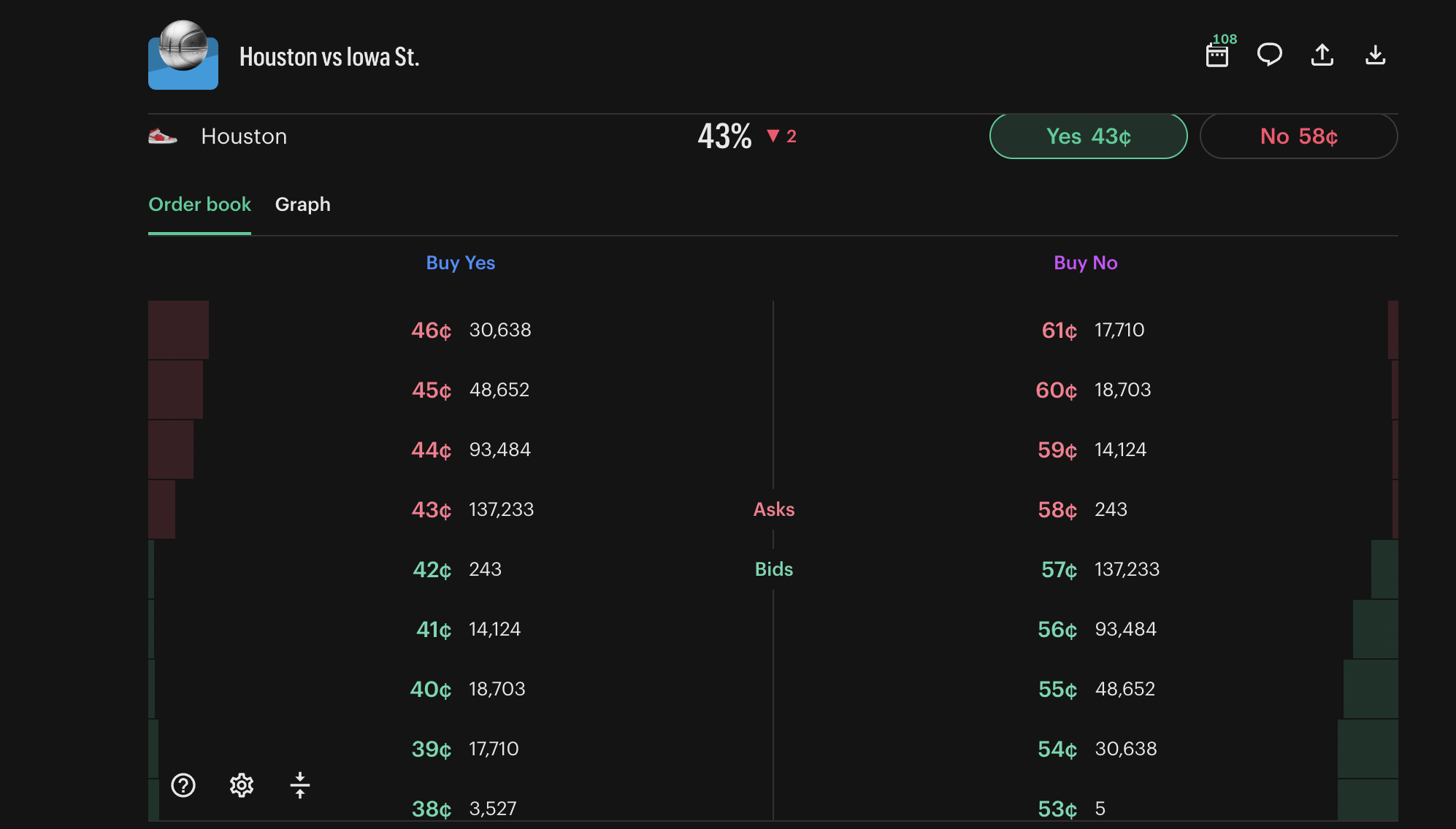

The layout difference is clear. Polymarket displays a single vertical book — asks stacked above bids, with a tab to toggle between yes and no. Kalshi shows both sides at once in parallel columns labeled “Buy Yes” on the left and “Buy No” on the right.

That side-by-side layout also makes the yes + no = $1 relationship easy to spot. Look at the numbers: the yes column shows 96,250 contracts at 43¢, and the no column shows 96,250 at 57¢. 43 + 57 = 100. Same thing at 45¢ and 55¢ — both show 61,092 contracts. They’re the same orders, just displayed from opposite sides.

Polymarket uses a hybrid model. Orders are matched off-chain for speed — meaning the matching engine runs on Polymarket’s servers, not on the blockchain — but settlement happens on-chain through smart contracts on Polygon.

Your positions on Polymarket are stored as tokens on the Polygon blockchain using the Conditional Tokens Framework. That means there’s a public record of who owns what. The trade itself happens fast on Polymarket’s servers, but the final settlement is recorded on-chain — so you get the speed of a centralized exchange with a verifiable receipt.

For most traders, the practical difference comes down to fees and incentives. On Polymarket, maker orders incur 0% fees across all markets. Taker fees currently apply only on 15-minute crypto, 5-minute crypto, NCAAB, and Serie A markets, and those fees are redistributed daily to makers through the Maker Rebates Program.

Taker fees scale with probability — they’re highest near 50% odds and drop toward the extremes, with a maximum effective rate of 1.56% at 50% probability on 15-minute markets and 0.44% on 5-minute markets. All other Polymarket markets remain fee-free.

On Kalshi, the fee formula of 0.07 × contracts × price × (1-price) applies to taker orders across all markets. Maker fees are lower, and rebates apply on select markets. The full breakdown is in our fees comparison.

These structural differences matter more for programmatic traders and market makers than for casual users. Placing a single $100 trade on a Super Bowl market? Both platforms feel the same. Running a strategy that depends on execution speed, fee optimization, or on-chain settlement verification? The architecture matters.

Once your order fills, the next thing that matters is what happens when the event resolves. That’s a different process on each platform — we break it down in how prediction market contracts settle.

How to use the order book to trade better

Everything above points to a handful of practical takeaways that apply regardless of which platform you trade on.

- Check depth before placing large orders. The displayed price is not your fill price if your order exceeds the available depth at the top of the book. Look at the full order book and estimate your average fill before you commit.

- Use limit orders on low-liquidity markets. Market orders on thin books guarantee slippage. A limit order lets you name your price and wait. You’ll also pay lower fees — or none at all on Polymarket.

- Watch the spread. A spread wider than 3–4¢ means you’re paying a meaningful premium for immediacy. It also means the market’s probability estimate is less precise than the displayed price suggests. On wide-spread markets, limit orders aren’t just cheaper — they produce better entries.

- Understand that limit orders make you a market maker. When you place a limit order, your resting order improves the book for every other trader. Platforms reward this: Polymarket pays daily USDC rebates on eligible markets, and Kalshi offers fee reductions. You’re not just getting a better deal — you’re contributing to the market’s efficiency.

- Factor order type into your strategy, not just your view on the event. Two traders with the same opinion on an outcome can get materially different results based on how they place their orders.

A taker order at 65¢ with 2% slippage and full taker fees is a meaningfully different trade than a maker order at 63¢ with no slippage and zero fees — even though both traders are betting the same direction.

The order book isn’t a detail you can afford to ignore. It’s the system that sits between your opinion and your P&L (profit and loss).