Kalshi and Polymarket sit at the top of the prediction market space, but they were built on entirely different foundations. Together they’re processing billions of dollars a week but these apps are not the same.

Much of the confusion is in Polymarket running two separate prediction markets under the same brand. Most of the coverage around Polymarket doesn’t distinguish between the two. The main Polymarket brand you see in the news is related to their offshore platform. Polymarket US, which is in beta, is a separate US product registered with the CFTC.

This Kalshi vs. Polymarket comparison provides an overview of all three and distinctly calls out the key differences. Below, you’ll find direct comparisons of fees, markets, rules, features and markets and how the US prediction market scene is vastly different from the international. Kalshi and Polymarket US are both operating in the US. Polymarket is not.

Trade $10, Get $10 Free

CODE: DEFI

World Cup markets: Halftime, groups, winner markets

Deposit $20, Get $50 Bonus

Must be 18+. Available for

Unless explicitly noted as Polymarket US, Polymarket will refer to the international version of the site which does not accept US traders.

| Category | Kalshi | Polymarket International | Polymarket US |

|---|---|---|---|

| What each platform is | CFTC-regulated DCM, USD-based centralized exchange | Decentralized, Polygon blockchain, USDC-based, global access | CFTC-registered beta relaunch via QCEX acquisition |

| Market coverage | 350,000+ markets; sports ~90% of volume | Politics, geopolitics, crypto, culture, sports | Sports only; access gated behind a waitlist |

| Volume and liquidity | $2.7B+ weekly (53% share); deepest in US sports | $2.1B+ weekly (47% share); deepest in politics and crypto | $5M+ weekly volume (0% share); 440 active markets; $650.3K open interest |

| Fees | $0.07 formula, capped at $1.75/100 contracts; no fees on politics | Zero (small fees on crypto markets from early 2026) | 0.10% taker-only flat fee |

| Currency and deposits | USD; bank, debit, crypto, Apple Pay, wire | USDC only; connected crypto wallet required | USDC only; no fiat support |

| Payouts and withdrawals | USD to bank or debit; settles within a few hours; hold periods apply | USDC to wallet; instant on-chain; off-ramp required for fiat | USDC to wallet; instant on-chain |

| Interest on balance | 3.75–4% APY on cash and open positions | None | None |

| Position limits | Up to $7M on select markets; $25K default for most | No fixed caps; liquidity-dependent | No fixed caps; liquidity-dependent |

| Resolution | Designated third-party sources per contract rules | Independent on-chain oracles | CFTC-registered; third-party source verification under DCM framework |

| Regulatory status | Full DCM designation since 2020 | Operates outside US jurisdiction | CFTC-registered, beta, maturing |

| Insider trading | CFTC-regulated; two documented enforcement cases in 2026; penalties and suspensions issued | No CFTC jurisdiction; no enforcement mechanism over international platforms | CFTC-regulated; same oversight framework as Kalshi |

| Conflict markets | Prohibited under CFTC rules; halted Khamenei market and reimbursed traders | Listed Iran strike and Khamenei markets; continued operating; outside CFTC jurisdiction | Prohibited under CFTC rules; did not offer Iran or Khamenei markets |

| Tax reporting | 1099-INT, 1099-MISC, 1099-B issued; FIFO accounting | No reporting infrastructure currently | In development; not yet in place |

What each platform is

| Operator | Notes |

|---|---|

| Kalshi | Centralized US exchange, CFTC-designated contract market since 2020, USD-denominated, available in all 50 states |

| Polymarket International | Decentralized protocol built on Polygon blockchain, USDC-denominated, global access, does NOT accept US traders |

| Polymarket US | CFTC-registered beta relaunch via QCEX acquisition; only has sports markets right now; beta access began November 2025 |

What is Kalshi?

Kalshi was the first prediction market platform to win federal approval to run event contracts as derivatives — not gambling products. That designation, granted by the CFTC in 2020, is what lets it operate legally in states where sports betting is still banned and why its contracts survive court challenges that would have shut down an unlicensed competitor.

Kalshi runs an order book across the US, allowing you to trade against other traders, not the house. Market availability ranges from economics to financial to sports. Sports contracts are currently geofenced in Massachusetts following a January 2026 preliminary injunction, with that litigation ongoing.

Learn more: Detailed Kalshi review

What is Polymarket?

Polymarket is a decentralized prediction market built on the Polygon blockchain where users trade on the outcomes of real-world events using USDC. There is no house — prices are set by traders buying and selling yes/no shares, with each contract paying $1 to the winning side on resolution.

Because it operates as a decentralized protocol outside US jurisdiction, Polymarket can and does list markets that regulated US exchanges cannot: war, assassination, geopolitics, crypto, culture, and long-tail global events that would never clear CFTC review. These markets are NOT accessible to US residents.

What is Polymarket US?

Polymarket spent $112 million last July to buy a CFTC license outright, acquiring QCEX, a registered exchange and clearinghouse. The CFTC issued its Amended Order of Designation on November 25, 2025 and Polymarket announced a beta launch in January 2026 with sports markets only. The site has yet to fully roll out to the US market and has a large backlog of waiting customers.

Learn more: Detailed Polymarket review

Market coverage

| Operator | Notes |

|---|---|

| Kalshi | 350,000+ active markets; sports, politics, economics, crypto; sports ~90% of volume; spread, totals, props, and combo contracts available |

| Polymarket International | Strongest in politics, geopolitics, and crypto; also covers culture, world events, earnings, and real estate |

| Polymarket US | Sports only; access gated behind a waitlist with hundreds of thousands of users pending; no public timeline for full launch or expanded categories |

| Which is better? | Kalshi is the better option for US traders right now. Polymarket for international. |

Kalshi lists over 350,000 active markets across sports, politics, economics, and crypto. Sports now accounts for roughly 90% of its trading volume, a shift that accelerated sharply with the 2025–26 NFL season.

Beyond game outcomes, Kalshi offers spread contracts, totals, player props, and a parlay-equivalent feature called Build Your Combo. Its political and economics markets — Fed decisions, CPI, inflation, elections — remain active but are secondary to sports in terms of raw volume.

Kalshi launched mention markets in fall 2025, which let users trade on whether specific words or phrases will appear in speeches, press conferences, or social media posts. These have since grown to volumes comparable to smaller sporting events. Trump mention markets have become increasingly popular across both platforms.

Polymarket’s category mix is genuinely distributed, with roughly 60% of volume coming from outside sports — politics, geopolitics, crypto, and long-tail global events all pull meaningful share.

Polymarket US launched with sports only and remains gated behind a waitlist. Hundreds of thousands of users are still waiting for access as of early 2026, with the company rolling out invites in batches but providing no public timeline for a full launch or expanded category range. Market coverage is limited to a handful of sports.

Volume and liquidity

| Operator | Notes |

|---|---|

| Kalshi | $2.7B+ weekly (53% share); deepest liquidity in major US sports contracts; institutional-sized orders absorbable in top markets |

| Polymarket International | $2.1B+ weekly (47% share); deepest liquidity in major political and crypto markets |

| Polymarket US | $5M+ weekly (0% share); 440 active markets; $650.3K open interest; transaction data not yet reported |

| Which is better? | Kalshi for US traders, Polymarket for international |

The numbers are hard to contextualize. Kalshi and Polymarket currently split the market roughly 53/47, with Polymarket US accounting for a fraction of a percent as it continues its beta rollout. For current figures, our prediction markets tracker updates hourly.

Combined, Kalshi and Polymarket produced $1.63 billion across Super Bowl 60 markets — the largest event window in prediction market history, with Super Bowl Sunday alone generating approximately $1.34 billion, the single largest trading day on record. The DeFi Rate tracker reflects rolling figures across all three platforms.

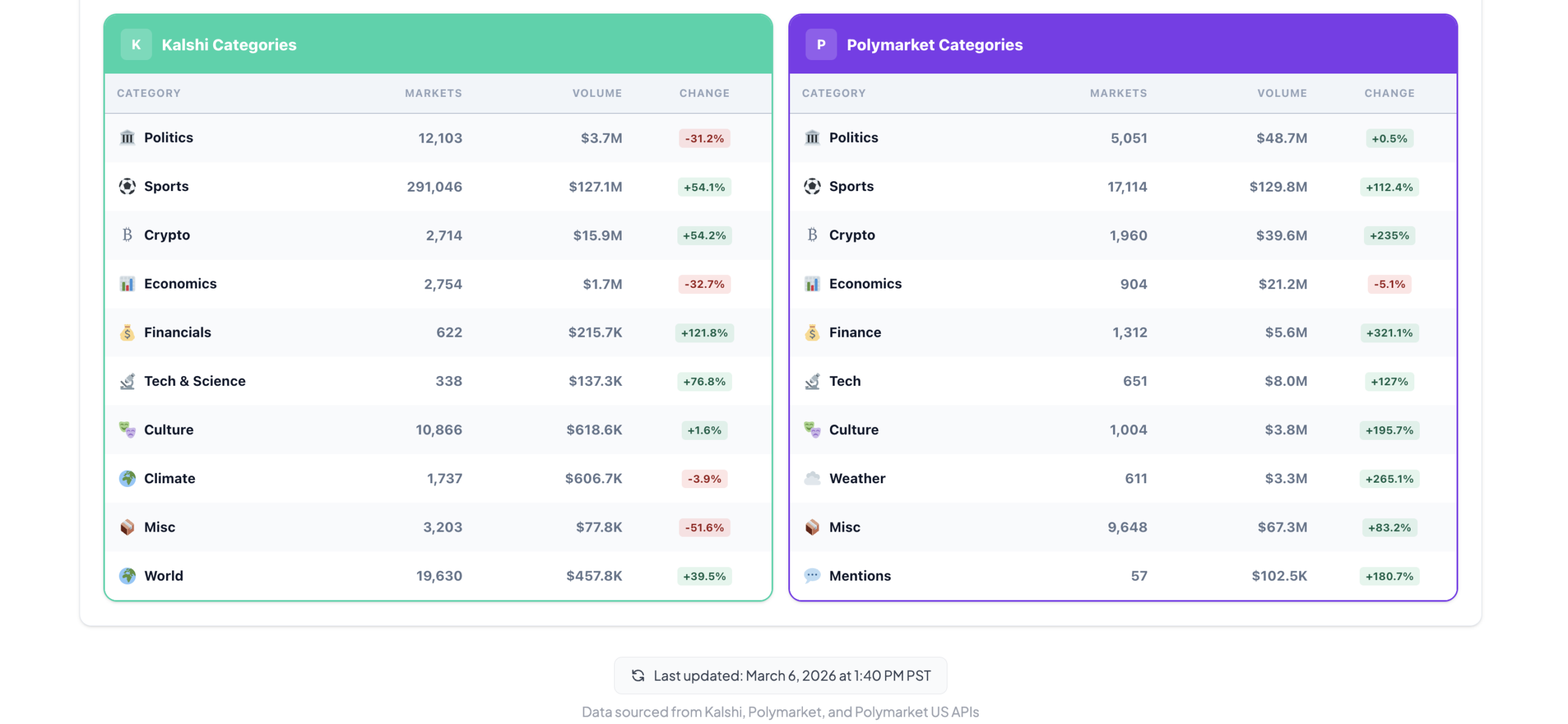

Liquidity is not evenly distributed, and the category snapshot below makes the contrast hard to ignore. On Kalshi, sports pulled $127.1M — roughly 84% of all volume — while crypto ($15.9M), politics ($3.7M), and economics ($1.7M) accounted for the tail. Institutional-sized orders are absorbable in top sports markets; thinner categories carry meaningfully less depth.

On Polymarket, no single category dominates. Sports led at $129.8M (~40%), but misc contracts added $67.3M (21%), politics $48.7M (15%), and crypto $39.6M (12%). Economics contributed another $21.2M.

Polymarket also offers minute markets — short-duration contracts, primarily on crypto prices, that resolve within 15 minutes. These carry a small taker-only fee introduced in early 2026, making them the only markets on the global platform where fees apply. Most standard markets remain zero-fee. Smaller markets on both platforms carry thinner order books, which affects how easily large positions can be entered or exited.

Fees

| Operator | Notes |

|---|---|

| Kalshi | $0.07 × contracts × price × (1-price), capped at $1.75/100 contracts (taker) and $0.44 (maker); highest near $0.50 contracts; no fees on politics markets |

| Polymarket International | Zero fees; small taker-only fees introduced on 15-minute crypto markets in early 2026 |

| Polymarket US | Flat 0.10% taker-only fee on total contract value |

| Which is better? | Polymarket US for sports, Polymarket international for everyone else |

Kalshi’s fee formula is: 0.07 × contracts × price × (1 − price), capped at $1.75 per 100 contracts for takers and $0.44 for makers. Because price appears as P × (1-P) in the formula, fees are highest on contracts priced near $0.50 and lowest near the extremes.

Polymarket has operated with zero trading fees since inception, with small taker-only fees introduced on 15-minute crypto markets in early 2026 as a deterrent to bot activity. Polymarket US charges a flat 0.10% taker-only fee on total contract value — lower than any competing regulated US exchange. For a full breakdown of how fees compare across platforms, see our prediction market fees guide.

Currency and deposits

| Operator | Notes |

|---|---|

| Kalshi | USD; bank transfer, wire, debit card, Apple Pay, crypto (BTC, SOL, USDC, WLD); crypto converts to USD on arrival via ZeroHash; 2% fee on debit/Apple Pay |

| Polymarket International | USDC only; connected crypto wallet required; no fiat support; funds via exchange or MoonPay on-ramp |

| Polymarket US | USDC only; no fiat support currently |

| Which is better? | Hands down Kalshi. You have all of the options available to you. |

Kalshi is a dollar-in, dollar-out platform. Funding options include bank transfer, wire, debit card, Apple Pay, and crypto (BTC, SOL, USDC, WLD). Any crypto deposited through partner ZeroHash is converted to USD upon arrival — your balance and all open positions are held in dollars. Debit card and Apple Pay deposits carry a 2% fee. Bank and wire transfers are free.

Polymarket operates entirely on crypto rails. Both the global platform and Polymarket US require USDC and a connected compatible wallet. There is no fiat deposit option on either version. For users coming from traditional banking, this is a meaningful barrier — funding a Polymarket account involves acquiring USDC through an exchange or on-ramp service before any trading can begin.

Payouts and withdrawals

| Operator | Notes |

|---|---|

| Kalshi | USD to bank or debit; settles within 2 hours; hold periods: 3 days (debit), 7 days (same-bank ACH), 30 days (different bank) |

| Polymarket International | USDC to wallet; instant on-chain settlement; no platform withdrawal fee; network fees may apply; fiat requires external off-ramp |

| Polymarket US | USDC to wallet; instant on-chain; fiat conversion requires external off-ramp |

| Which is better? | Kalshi. You have access to all tax forms |

Kalshi contracts typically settle within a few hours of an event resolving — sports markets often resolve faster, while complex political markets requiring manual verification can take longer. Winnings land in your cash balance in USD and can be withdrawn by ACH, debit card, or crypto. The hold structure is worth noting: debit card deposits are held for three days before withdrawal is available, bank transfers for seven days if withdrawing to the same bank, and 30 days if withdrawing to a different bank.

Polymarket settlement is instant once a market resolves. Winning USDC moves back to your wallet on-chain with no platform withdrawal fee, though standard network fees apply. Getting those funds to a bank account requires an additional step through an off-ramp exchange, as Polymarket does not handle fiat conversions directly.

Interest on balance

| Operator | Notes |

|---|---|

| Kalshi | 3.75–4% APY on cash and open positions; accrues daily, pays monthly; minimum $250 balance required |

| Polymarket International | None |

| Polymarket US | None |

| Which is better? | Kalshi, since there are no reward incentives elsewhere. |

Kalshi pays 3.75–4% APY on your total balance, including funds tied up in open positions. Interest accrues daily based on end-of-day portfolio value and pays out monthly. A minimum balance of $250 is required to qualify. The rate is variable and subject to change.

Neither version of Polymarket pays interest on held balances. Your USDC earns nothing while it sits in a connected wallet waiting to be deployed.

Position limits

| Operator | Notes |

|---|---|

| Kalshi | Up to $7M on select high-profile markets; $25K default for most markets |

| Polymarket International | No fixed caps; constrained by available liquidity |

| Polymarket US | No fixed caps; constrained by available liquidity |

| Which is better? | Both are equal |

Kalshi allows positions up to $7 million per market on select high-profile markets — the default limit on most markets is $25,000, with Eligible Contract Participants able to access higher thresholds. In top-tier markets, the limit is sufficient for institutional-sized positions.

Polymarket imposes no fixed position caps. Your practical limit is determined by available liquidity in the market you’re trading. In deep markets, this can support very large positions. In thin markets, it creates meaningful slippage risk.

Resolution

| Operator | Notes |

|---|---|

| Kalshi | Designated third-party sources specified per contract (e.g., AP, Fox Sports, ESPN); disputes handled through CFTC-regulated process |

| Polymarket International | Independent on-chain oracles; outcome verification via publicly available data; disputes resolved through community and oracle governance |

| Polymarket US | CFTC-registered; third-party source verification under DCM framework |

| Which is better? | Kalshi. Polymarket has a history of not changing outcomes |

Kalshi designates specific third-party sources in the rules of each contract — for a pro football championship market, that might be AP, Fox Sports, and ESPN. If those sources confirm an outcome, the contract settles. Traders can review the exact sources and settlement logic before placing a trade, and Kalshi’s oversight means disputes go through a regulated process.

Polymarket resolves markets through independent on-chain oracles that verify outcomes using publicly available data. The decentralized model means no single entity controls resolution, but disputes play out through community and oracle governance rather than a regulatory framework. The oracle model means resolution is transparent and auditable by anyone; the Kalshi model means resolution authority sits with a regulated exchange that has accountability to the CFTC.

Regulatory status

| Operator | Notes |

|---|---|

| Kalshi | Full CFTC DCM designation since November 2020; event contracts classified as derivatives, not gambling; federal courts have consistently upheld jurisdiction |

| Polymarket International | Founded June 2020; CFTC settlement January 2022 ($1.4M fine); exited US market January 2022; operates outside US jurisdiction as a decentralized protocol |

| Polymarket US | QCEX acquired July 2025 ($112M); CFTC no-action letter September 2025; Amended Order of Designation November 25, 2025; beta access began November 2025; sports markets only |

Kalshi holds full DCM designation from the CFTC — the same regulatory classification as traditional commodity exchanges like the CME. That status means its event contracts are classified as derivatives, not gambling, which is why Kalshi operates legally in states where sports betting isn’t legal. Federal courts have consistently upheld this position, including a recent California ruling that dismissed tribal efforts to block Kalshi’s sports contracts.

Polymarket operates outside US jurisdiction as a decentralized protocol. Its market outcomes are governed by on-chain oracles rather than a regulated clearinghouse. On the flip side, Polymarket US is building toward full CFTC compliance through the QCEX acquisition.

Insider trading

| Operator | Notes |

|---|---|

| Kalshi | CFTC-regulated; two documented enforcement cases; actions announced February 2026; penalties and suspensions issued in both |

| Polymarket International | Outside CFTC jurisdiction; no regulated intermediary; on-chain data is auditable but there is no enforcement mechanism |

| Polymarket US | CFTC-regulated; subject to same oversight framework as Kalshi |

Insider trading is an open structural question for prediction markets, and the two platforms sit on opposite ends of the enforcement spectrum. On February 25, 2026, Kalshi announced both enforcement actions simultaneously, and the CFTC Enforcement Division issued a formal advisory the same day.

The first involved Kyle Langford, a longshot Republican candidate in California’s governor’s race, who bet approximately $200 on his own candidacy and then posted a screenshot of the trade on X — a case Dustin Gouker at The Event Horizon had first reported nine months earlier, noting that Langford had essentially reported himself. Kalshi’s surveillance system flagged the activity, froze his account the same day, and contacted him — Langford acknowledged the trades violated exchange rules. Kalshi imposed a $2,246.36 penalty ($246.36 in disgorgement plus a $2,000 fine) and a five-year suspension, with the fine earmarked for donation to a nonprofit providing consumer education on derivatives markets.

The second involved a MrBeast channel editor, Artem Kaptur, who traded a prediction market tied to the channel he worked for between August and September 2025, using advance knowledge of video content before it was publicly posted. Kalshi concluded the trades were based on material non-public information and imposed a $20,397.58 penalty — $5,397.58 in disgorgement plus a $15,000 fine — and a two-year suspension.

Kalshi and Polymarket US carry regulatory exposure and a formal obligation to investigate suspicious activity. Neither platform has implemented a public, systematic surveillance process comparable to what exists in traditional financial markets.

Conflict markets

Conflict markets are prediction contracts geared towards geopolitical events involving war, military action, assassination, or the fate of foreign leaders. Under CFTC Regulation 40.11, registered entities including designated contract markets like Kalshi and Polymarket US are prohibited from listing contracts that involve, relate to, or reference war, terrorism, or assassination. Offshore platforms like Polymarket operate with their own rules and have listed war and assassination contracts freely. This is why the same event can produce different outcomes on each platform, and why the media and regulators routinely conflate the two.

| Operator | Notes |

|---|---|

| Kalshi | Prohibited from listing war and assassination contracts under CFTC rules; halted Khamenei market on February 28, 2026; settled pre-death positions at last traded price rather than $1 |

| Polymarket International | Listed Iran strike and Khamenei markets; Khamenei market resolved YES and paid out; offshore and outside CFTC jurisdiction |

| Polymarket US | Prohibited from listing war and assassination contracts under CFTC rules; did not offer Iran or Khamenei markets |

When US and Israeli forces killed Khamenei on February 28, 2026, both platforms had active markets on his ouster. Polymarket’s contract resolved YES and paid out $529 million in full — no CFTC death restriction applies offshore. Kalshi halted its market, settling $21.7 million in positions at the last traded price before death rather than $1, triggering widespread trader backlash. The company acknowledged its settlement language was “grammatically ambiguous” and reimbursed fees. CEO Tarek Mansour wrote on X: “We don’t list markets directly tied to death. When there are markets where potential outcomes involve death, we design the rules to prevent people from profiting from death.”

Separately, Bubblemaps flagged six Polymarket wallets — all funded within 24 hours of the strikes — that made a combined $1.2 million on the Iran strike contracts.

Senator Chris Murphy responded on X: “It’s insane this is legal. People around Trump are profiting off war and death. I’m introducing legislation ASAP to ban this.”

Senator Adam Schiff, who had led six senators in a pre-strike letter to the CFTC warning about contracts tied to death and assassination, posted after Khamenei’s death: “Gambling on war and death doesn’t just present national security risks, it also raises serious concerns about potential insider trading — presenting unscrupulous government officials with a chance to profit off the new war in Iran. These contracts are immoral. @CFTC can and must ban them.” Both were responding to activity on Polymarket, whose offshore structure is not the same as Kalshi and Polymarket US.

Mansour pushed back directly, telling Murphy in two separate posts: “The market you’re posting is unregulated and offshore” and “Regulated prediction markets are not allowed to do war markets.”

Tax reporting

| Operator | Notes |

|---|---|

| Kalshi | Issues 1099-INT, 1099-MISC, 1099-B; FIFO accounting; monthly P&L data available; IRS classification of trades still unresolved |

| Polymarket International | No reporting infrastructure; tax treatment depends on individual jurisdiction and trader recordkeeping |

| Polymarket US | 1099 forms expected as platform matures; not yet in place |

| Which is better? | Kalshi. Polymarket does not provide the documents needed yet |

Kalshi reports trading activity to the IRS and issues three tax documents: a 1099-INT for interest earned on balances, a 1099-MISC for bonuses and credits, and a 1099-B for crypto transfer proceeds — note the 1099-B covers crypto transactions only, not general event-contract trading activity. Gains and losses are calculated using FIFO accounting, and monthly P&L data is available through the platform.

Polymarket US is expected to issue 1099 forms as the platform moves out of beta, but how tax reporting will work in practice is not yet known. For traders on the global platform, tax treatment depends entirely on individual jurisdiction and the trader’s own recordkeeping. Kalshi’s tax documentation is clear, while Polymarket’s is a work in progress and requires recordkeeping if transferring from crypto assets. See our crypto tax calculator to learn more.