- ▸ Polymarket is weighing a ~$400M raise at a $15B valuation, but hasn’t locked pricing as it debates timing vs. upside.

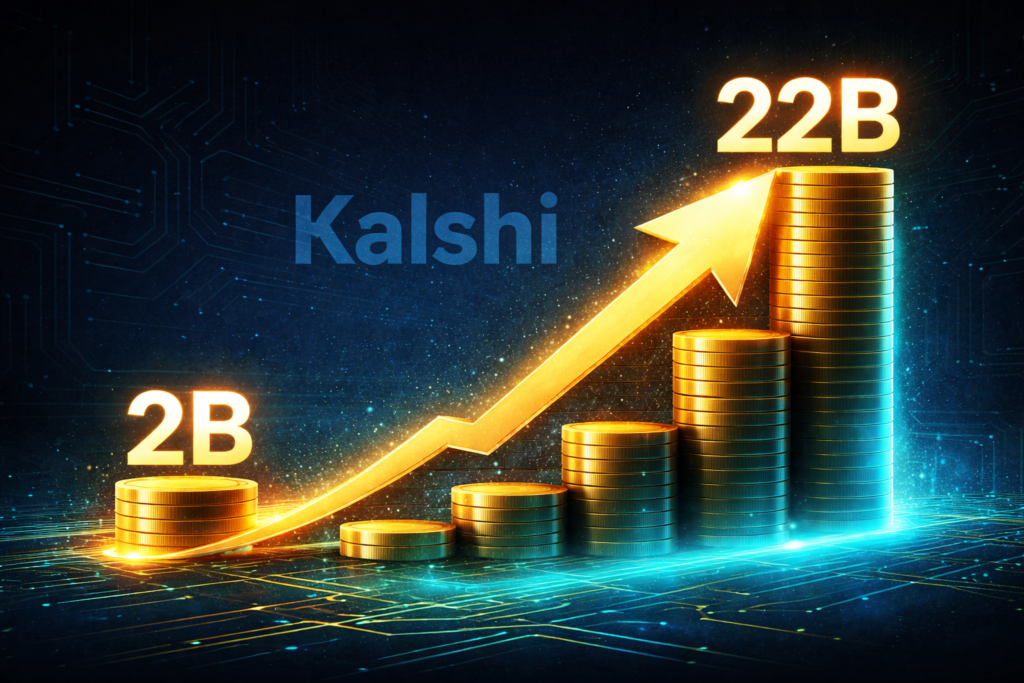

- ▸ Kalshi has surged to a ~$22B valuation after multiple rapid raises, widening the gap while pulling ahead in trading volume.

- ▸ Valuations weigh growth vs. risk amid Polymarket offshore controversies and ongoing US legal challenges.

Polymarket is reportedly weighing a new funding round that could value the prediction market platform at around $15 billion, as the company considers whether to raise additional capital now or hold out for a higher price.

The valuation, first reported by The Information and later corroborated by Bloomberg, would mark a significant increase from the roughly $9 billion level established in Polymarket’s October 2025 funding deal with Intercontinental Exchange (ICE), but it also falls within a range the company has been linked to for months. Since that round, different reports have suggested that Polymarket was exploring valuations between $12 billion and $20 billion, including a March Wall Street Journal report that placed it alongside rival Kalshi in targeting the upper end of that range.

Bloomberg reported that Polymarket is now considering whether to raise approximately $400 million at the $15 billion level, which would include the new capital, or delay fundraising in hopes of securing a higher valuation. The deliberation suggests the company has yet to lock in a new price despite strong growth in trading activity and revenue following recent product and monetization changes.

Since late 2025, the two top prediction market platforms have followed divergent paths in how their valuations have evolved.

Polymarket hasn’t announced new funding since October

Since Polymarket’s last priced round, Kalshi has completed two funding raises, first reaching an $11 billion valuation in December and then $22 billion in a March round, shortly after the WSJ report, marking a rapid repricing in just a few months.

Polymarket’s most recent pricing event came in October 2025, when ICE announced plans to invest up to $2 billion, including an initial $1 billion stake, in a deal that valued the company at about $9 billion post-money. After the ICE investment, CEO Shayne Coplan revealed previously undisclosed funding rounds. Coplan wrote on X that a 2024 round led by Blockchain Capital raised $55 million at roughly a $350 million valuation. He also said that an earlier 2025 round raised $150 million at about a $1.2 billion valuation.

ICE continued to add to its position, including a $600 million investment in March, bringing its total investment to roughly $1.6 billion and completing its commitment under the deal, according to the company. However, those follow-up investments did not establish a new valuation.

Kalshi, by contrast, has repriced multiple times over the same period, climbing from a $2 billion valuation in June 2025, when it raised $185 million in a Series C round led by Paradigm. The company was then valued at around $5 billion in October following a $300 million raise led by Andreessen Horowitz, before raising $1 billion in December (again led by Paradigm) at an $11 billion valuation. In March, Kalshi reportedly secured another roughly $1 billion round, led by Coatue Management, at a $22 billion valuation.

The divergence is notable given that, in March, both companies were reportedly targeting valuations of up to $20 billion.

Trading volumes reflect intensifying competition

Both platforms have seen rapid growth in trading activity in 2026, with monthly and weekly volumes climbing alongside rising interest in prediction markets.

Recent data shows the gap narrowing at peak moments. In March, Kalshi and Polymarket each processed roughly $12 billion in trading volume, with Kalshi holding a narrow edge. The near-parity marks one of the closest monthly results between the two platforms to date and shows how competitive the market has become during peak periods like the NCAA tournament.

Kalshi vs. Polymarket Last 6 Weeks (March 9 – April 19)

| Week | Kalshi Volume ($) | Polymarket Volume ($) | Kalshi Transactions | Polymarket Transactions |

|---|---|---|---|---|

| 2026-03-09 | $2.93B | $2.34B | 19.7M | 24.7M |

| 2026-03-16 | $3.40B | $2.54B | 21.4M | 27.4M |

| 2026-03-23 | $2.73B | $2.24B | 19.0M | 26.3M |

| 2026-03-30 | $2.90B | $1.97B | 20.1M | 22.7M |

| 2026-04-06 | $3.54B | $2.48B | 22.2M | 22.3M |

| 2026-04-13 | $3.06B | $2.04B | 20.9M | 21.4M |

Even so, Kalshi has continued to lead over longer timeframes. As of April 20, its year-to-date trading volume stood at roughly $37.49 billion, compared to about $29.23 billion for Polymarket.

The result is a tightening race in which Polymarket is matching Kalshi at peak demand but still trailing in sustained volume.

Polymarket gets heat for suspicious trades on international platform

Beyond trading volumes, the two platforms have faced very different regulatory challenges over the past year.

Kalshi has been drawn into a series of legal disputes with state regulators over its sports event contracts, with states arguing the markets are sports betting and fall under existing, state-level gambling laws. The Commodity Futures Trading Commission (CFTC), which oversees U.S. prediction market trading, has intervened in several of those cases, backing Kalshi’s position that federally regulated exchanges fall under its exclusive jurisdiction.

Polymarket, by contrast, operates primarily through an offshore platform that is not available to U.S. users nor overseen by the CFTC. Insider trading concerns tied to geopolitical and U.S. policy markets have generated headlines in recent months, with many of the widely-cited, questionable trades occurring on Polymarket’s international platform. The attention has even drawn scrutiny from members of Congress. In a recent letter, lawmakers urged the CFTC to examine offshore prediction markets and consider whether its authority under the Commodity Exchange Act can be used to address those risks.

Those concerns were raised directly during a House Agriculture Committee hearing on April 16 in which committee members questioned CFTC chair Mike Selig. When asked whether the agency needed additional authority to respond to questionable offshore trading activity, Selig said that the CFTC’s extraterritorial authority is “fairly broad,” particularly in swaps markets, but acknowledged that its reach is more limited in futures and could be expanded.

The contrast points to a split between a platform operating inside the U.S. regulatory framework and one that has grown largely outside of it, a difference that could factor into how investors assess risk across the sector.

Polymarket monetization and product expansion offer upside

Despite the scrutiny, Polymarket has also made several moves that point to a more mature and potentially more investable business model.

Most notably, the platform has begun capturing significantly more revenue from its international exchange. A late-March expansion of trading fees across most market categories marked a shift away from its earlier no-fee structure, driving a sharp increase in monetization. Daily revenue climbed from roughly $30,000-$80,000 in January to about $550,000-$700,000 in early April, with peak days reaching even higher levels following the fee rollout.

Importantly, that shift has not slowed trading activity. Volume continued to rise alongside the fee expansion, suggesting the platform may have found a way to increase revenue without materially impacting user demand.

At the same time, Polymarket has taken steps to address the very concerns that have drawn headlines and scrutiny. In March, the company published enhanced market integrity rules across both its international platform and its CFTC-regulated U.S. exchange, explicitly prohibiting trading based on stolen confidential information, illegal tips, or positions of influence over an outcome. The updated framework also introduced clearer enforcement guidelines and reporting mechanisms aimed at identifying suspicious activity.

Its U.S. product has also shown more signs of traction recently. Polymarket US recorded $256 million in trading volume in March and has begun expanding beyond just sports markets.

Those developments point to a company that is not only growing its volume, but also improving its ability to monetize activity, expand its product suite, and respond to integrity concerns, factors that could support a higher valuation over time.

Valuation gap reflects more than just growth

The divergence in valuations points to a market that is still deciding how to price growth against risk. Polymarket has shown it can scale, monetize, and expand its product offering, but Kalshi has been able to convert its position into successive funding rounds at higher valuations.

For now, that gap suggests investors are favoring platforms with clearer regulatory footing and more consistent execution, even as competition between the two continues to tighten.