A trader says he lost $500,000 on Polymarket after the platform rewrote the resolution conditions of a $175.2 million market after an SEC filing confirmed MicroStrategy had sold 32 Bitcoin before the May 31 deadline.

The case has exposed two compounding problems: a platform willing to alter market intent after the fact, and a decentralized oracle resolution system that critics say is now effectively controlled by a small bloc of anonymous token holders with direct financial stakes in the outcomes they’re voting on.

MicroStrategy’s SEC form 8-K, filed June 1, disclosed a sale of 32 BTC for $2.5 million at an average price of $77,135 during May 26–31. The market, one in a series asking whether Michael Saylor’s company would sell any of its Bitcoin holdings by a given date, spiked to 81% for Yes within hours of the filing. Then Polymarket posted a clarification tying resolution to when a sale was confirmed, not when it occurred. The price collapsed to near zero.

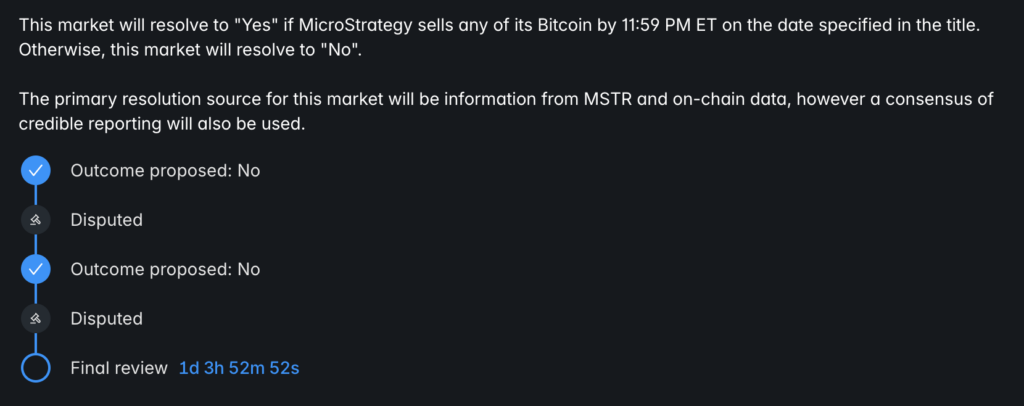

Once the market went into dispute, Polymarket’s highly controversial UMA oracle resolution system proposed the market resolve to “No,” which has been disputed twice and is currently still in dispute.

“I was just scammed for $500K by Polymarket,” trader willo2 (@willo2_Poly) wrote in a thread that has since drawn over 1.5 million views.

While the main contention in this particular case is with the rules change after millions had already been traded, the UMA oracle system still plays a key role. It’s a system that is broken by design, and has been for quite some time, according to many traders. Also worth noting that the resolution system here is completely different from what you get on CFTC-regulated exchanges like Kalshi, which have a federal regulator to answer to, based on commodities law, though those are not immune to controversial resolutions either.

Microstrategy market dispute details

The trader in question, willo2, says he started building his position a few days before the 8-K when MicroStrategy deposited approximately $30 million in Bitcoin to a Coinbase Prime hot wallet, a move he flagged as unprecedented based on his own on-chain research. He entered with initial Yes contracts at $5K, and in his own words, was watching closely.

When the company’s 8-K dropped on June 1 confirming the sale, the market, which was still open and trading, jumped. The trader scaled up aggressively, ultimately becoming the top holder of Yes contracts on the market.

“I reread the rules. SALE before May 31st. Reread the 8K. Microstrategy SOLD Bitcoin. The market was open and trading. So I jammed,” he wrote.

I was just scammed for $500K by Polymarket.

— willo2 (@willo2_Poly) June 2, 2026

I am "willo2", the top holder of YES on "MicroStrategy sells Bitcoin by May 31st".

Here's what happened: pic.twitter.com/4n81IdvLXI

The written rules were unambiguous: “This market will resolve to ‘Yes’ if MicroStrategy sells any of its Bitcoin by 11:59 PM ET on the date specified in the title. Otherwise, this market will resolve to ‘No.'” The primary resolution source was listed as information from MSTR and on-chain data, with consensus of credible reporting as a secondary source.

After the 8-K confirmed the sale and the market jumped to 81% for Yes, Polymarket posted the following “Additional context,” timestamped June 1, directly to the market’s rules page: “No information from MSTR, on-chain data, or consensus of credible reporting confirmed that MicroStrategy sold Bitcoin within the market’s timeframe. Confirmation achieved outside of the market’s time frame does not qualify.” The trader posted the following annotated market timeline on X:

The market is now sitting at less than 1% Yes, and is still in review. The outcome has been proposed as No, which was disputed, then followed by the same proposed outcome. In dispute again, the market lists a final review period with just over a day remaining at time of writing.

Late-game market clarification

The trader pointed out that “Polymarket specifically waited until the 8-K was filed to resolve the market,” and explicitly raised suspicion of foul play on the part of exchange insiders. “Their ‘sharps’ could fill 6-figures against people betting on a confirmed outcome, then they could add a new rule and scam all the newcomers.”

He also pointed to the resolution timing as further support for the rule change not aligning with market intent. “This was straight-up NOT part of the rules. It was not written down on the market, it did not make sense — and most of all, Polymarket didn’t even believe it themselves. Why? Because if it was true, the market would have closed on May 31st. The market didn’t close.”

Another affected trader, 0xDinosaur (@0xDinoCrypto), who held approximately 49,695 YES contracts for around $35,000 USDC, posted a formal public statement:

“The written rule said the market resolves YES if MicroStrategy sells any of its Bitcoin by the date in the title. It did not clearly say the sale had to be publicly disclosed by May 31, filed in an 8-K by May 31, or confirmed before the deadline. A sale date and a disclosure date are not the same thing.”

He went on to add: “If Polymarket intended this to be a disclosure-based market, the rule should have said so clearly. Ordinary users read ‘sells any Bitcoin by May 31’ as an event-based condition, not a disclosure-timing condition. Any ambiguity was created by the market wording itself.” 0xDinosaur confirmed he’s pursuing the matter through legal channels.

The June 30 and December 31, 2026 versions of the same MSTR market series have already resolved Yes, meaning Yes holders for the later timelines have already cashed in.

The UMA oracle lingering in the background

To understand the larger issues at play in this dispute, it’s important to understand how Polymarket resolves contested markets, and where the breakdown actually occurred here. Polymarket uses UMA (Universal Market Access), a decentralized “optimistic oracle” protocol that Polymarket uses to verify real-world data and resolve markets and settle disputed outcomes. When a resolution is challenged, UMA token holders vote on how the market should resolve. In this case, the UMA was triggered when the dispute arose, following the exchange’s market clarification on June 1.

More UMA tokens means more voting power. Voters are rewarded for siding with the eventual winning outcome and penalized for voting against it, a design intended to incentivize consensus, but one that in practice rewards following the largest voting bloc rather than settling on an objective truth.

According to a recent Bloomberg analysis (paywalled), “Just nine wallets accounted for roughly half of all UMA tokens that have voted on a Polymarket resolution over the past three years.” The same report also noted that “The nine wallets have essentially always voted together and for the winning position.”

As “cryptopunk” (@xcryptopunk) explained in a post, “disputes often become less about determining what happened and more about predicting where the largest voting blocs will land.”

a $20B company

— cryptopunk (@xcryptopunk) June 2, 2026

billions of dollars in prediction markets

and disputed outcomes are effectively decided by 9 UMA wallets.

Bloomberg found that over the past year, nearly 2,000 Polymarket contracts were disputed through UMA

in April 2026 alone, 230 disputed markets representing… https://t.co/ny74gY3JY7 pic.twitter.com/WsXIJKLwiD

Bloomberg also reported that the plans to “improve or replace the [UMA] process” that Polymarket and the team behind UMA, Risk Labs, confirmed last year are now on hold.

“Eigen Labs, which was working with Polymarket and Risk Labs on the update, said the project has been put ‘on pause.'” Sreeram Kannan, Eigen Labs’ founder, told Bloomberg: “The focus has been on market expansion from Polymarket’s end. We haven’t actually been working on that for the last several months.”

Polymarket did not respond to a request for comment.

A new UMA problem

The UMA oracle has long been contentious, but shifts in the voter makeup have only complicated matters. Enter UMA.rocks, a DeFi protocol that aggregates UMA token voting power by incentivizing delegators with double-digit APR % in exchange for automated voting. Their landing page currently reads: “Earn 21.12% APR by delegating your Polymarket voting power.”

UMA.rocks members vote on markets they have positions in, a structural conflict of interest that Domer (@Domahhhh), a well-known professional trader on Kalshi, documented in detail in an April 30 post that has taken on new relevance:

“The largest and most influential voter in the “oracle” that governs Polymarket’s prediction market is no longer anyone with Risk Labs (UMA was created by a legit crypto company, but they’ve stopped updating UMA and largely abandoned it). It is now UMA Rocks, a collection of Polymarket traders. UMA Rocks decisions are made by various unqualified bozos, who have real-money positions in the markets they’re voting to resolve, and thus have a strong incentives in resolving markets to something that personally benefits them.”

Hopefully Polymarket is on precipice of replacing UMA, because the "oracle" that underpins the site is now a disinformation engine that has been taken over by rogue traders.

— Domer❤️🔥 (@Domahhhh) April 30, 2026

(If you find the below post confusing, byzantine, stupid, or anything else, first of all that's probably… pic.twitter.com/Z9mtuKsW2O

Some users pointed out that the core issue in this instance was not a controversial UMA ruling, but rather an unfair rules change after-the-fact, that forced the resolution to No. And while it’s true that the rules clarification was issued independently of the UMA resolution protocol, the two are still interconnected. The clarification went to UMA voters, who are now being asked to vote based on Polymarket’s revised rules rather than the original ones.

As “EmeraldEdge” (@th33m3rald3dg3) put it: “What the Polymarket clarification did was: 1. Change the intent of the question by making the market more about the announcement than for the actual event occurring. 2. Gave the UMA voters who are the same No holders the reason to resolve contrary to rules and reality.” willo2 had a similar observation: “UMA might have settled it Yes due to the initial market rules but now they’re forced to vote on Polymarket’s changes. The clarification completely twists UMA’s arm.”

Polymarket’s own documentation states that clarifications “cannot change the fundamental intent of the question.” The market in dispute asked whether MicroStrategy sells Bitcoin by a certain date, which it undeniably did. Whether or not rewriting that into a disclosure-timing condition violates that clause is not really the question. The UMA voters are asked to rule on the updated market rules, which they already have done, even if the verdict isn’t yet finalized.

A “broken system”

Domer has been trading prediction markets long enough to know the difference between a bad beat and a broken system. He shared his verdict on the MSTR resolution:

“I do agree it was a scam. Although I think it’s wrong to blame it solely on Polymarket (even tho they’re def also to blame). UMA/UMA Rocks/hidden precedents/clarifications on vibes….It’s a totally, totally broken system where scams are now a regular occurrence. It is comically broken at this point. And it’s not funny at all when you’re the victim.”

His philosophical critique points to a larger issue: “The point of a prediction market is predicting what will happen. Anyone who predicted Yes was correct. Expiring it to No, which is a total lie, is a joke. It overturns the whole point of betting on the future.”

Co-founder and CEO of GensynAI Ben Fielding weighed in with an AI-based solution to resolution that removes the human element: “Stake-weighted human voting for settlement of prediction markets is ineffective. Verifiable and neutral AI settlement with chain consensus is the only way to scale this.”

While Polymarket’s own CEO Shayne Coplan has admitted shortcomings with the permissionless oracle, plans to improve or replace it may now be on pause. The disputed markets, meanwhile, continue to pile up. Moving the goalposts late in the game will only give the current token holders more power and with it, more financial incentive.

The MicroStrategy market debacle is a prime reminder of the risks traders are assuming, especially with Polymarket operating outside of federal jurisdiction and with a resolution system based on a small group of anonymous token holders.

0xDinosaur acknowledged the risk calculus but understandably wants Polymarket to abide by its own rules of not unfairly altering the “fundamental intent” of a market. “I accept that I took risk. My position was aggressive, and maybe I was greedy. But risk-taking does not change the facts, and it does not allow a platform to apply an unclear or unwritten rule after real money has already been placed.”