- ▸ Prediction markets let you trade the event itself rather than a proxy, meaning you can be right about an outcome and actually profit, unlike traditional hedges that can fail even when your thesis is correct.

- ▸ From Citadel Securities eyeing market-making opportunities to block trades in the $20–30M range, prediction markets are quietly shifting from “betting platforms” to legitimate risk management infrastructure.

- ▸ What might require a $50–100M bond position can be replicated with ~$670K in a prediction market contract, making them attractive for hedging macro, geopolitical, and regulatory risks with far less capital.

Prediction markets are pulling in institutions like a magnet for cleaner real-world hedging. Citadel Securities, one of the world’s largest market makers, has just revealed it is actively monitoring the space, pointing to event-based contracts as a new way to hedge real-world risks like elections and macro shocks.

And it’s not hard to see why. Hedge funds trying to hedge against a backed-up Strait of Hormuz have had their positions wiped out in real-time, all despite being right about the event. Even though the situation has driven global oil prices through the roof, the US stock market shockingly hit new all-time highs last week, punishing short-sellers.

The example illustrates a problem with hedging via traditional markets. It’s also why prediction markets are quickly gaining popularity among institutional investors.

Citadel Securities president says firm could enter prediction markets, eyes non-sports use caseshttps://t.co/HaK2hGlpY9

— Frank Chaparro (@fintechfrank) April 17, 2026

You can be right and still lose

When it comes to traditional hedges, you’re rarely trading the thing you actually care about. More often than not, you’re trading a proxy and hoping it reacts the way you expect. But it’s frustrating when those hedges go against you, even if you’re right about the event you were trying to hedge against.

That’s where prediction markets come in and flip the script completely, by letting you trade the event directly. Rather than relying only on trading loosely related assets, you can trade the event outcome itself. That means higher capital efficiency, clearer risk exposure, and more predictable payoffs.

Kalshi is one of the first prediction market platforms seriously attempting to meet institutional needs for exactly this purpose, recently securing a license for margin trading. The move is the first of many that aim to make the platform far more usable for sophisticated capital. As more institutional players enter, prediction markets will continue to break away from their “betting platform” reputation, and enter a new era of real-world risk management. As well-known entrepreneur and investor Anthony Pompliano put it, “There is no other way to isolate individual data points and make binary bets.”

Prediction markets are going to become the venue of choice for many of the largest capital allocators in the world.

— Anthony Pompliano 🌪 (@APompliano) April 16, 2026

There is no other way to isolate individual data points and make binary bets.

Don’t underestimate the gambling obsession of Wall Street.

Below, we break down seven ways prediction markets can already be used to manage institutional-scale risk.

Oil shocks, shipping disruptions and geopolitical events

A currently relevant potential use case for prediction markets is hedging against major global events. Typically, these have been hedged against via instruments like bonds, FX, commodities, or shorting equities.

But as we’ve seen, the problem is the event itself and outside factors can move those assets in unpredictable ways. To make matters worse, they often take a lot of capital to capture a small percentage move.

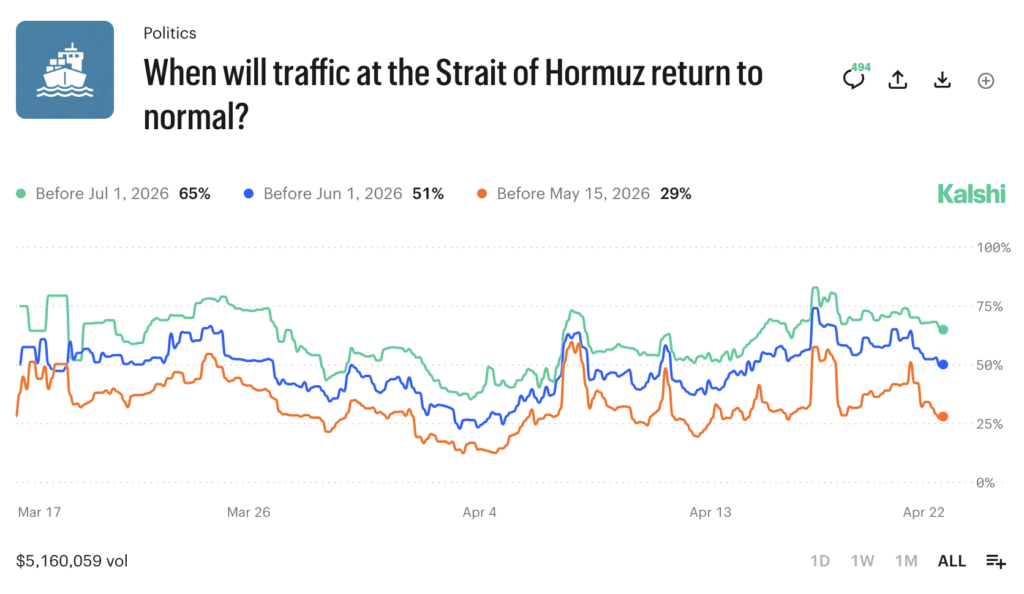

That’s where prediction markets are different. Rather than shorting equities or trading oil futures, prediction markets like Kalshi’s “When will traffic at the Strait of Hormuz return to normal?” offer a far more direct hedge.

Coinbase CEO Brian Armstrong made a case for exactly this type of hedge earlier this year, in a Bloomberg interview at the World Economic Forum. While discussing emerging uses of prediction markets, he pointed to simple, outcome-based questions:

“It could be on a political election… it could be, ‘Is the Suez Canal going to be reopened?’ Because I need to understand if I can put my ships through there as a multinational.”

Here we are months later, where a closely related scenario has presented itself.

One trade, one outcome

A macro fund no longer needs to express a rate view through just bonds anymore. Instead of just trading around a potential Federal Reserve rate cut, it can also trade the outcome itself by buying prediction market contracts.

An importing business worried about supply chains can hedge a potential event directly, rather than guessing how markets will react to geopolitical tensions.

What could’ve previously been messy hedge could now become one trade, one outcome, without the need to worry about second-order effects or unrelated market moves.

| Scenario | Traditional hedge | Prediction market hedge |

| Will the Strait of Hormuz close? | Short equities or trade oil | Buy “Hormuz closes” |

| Will rates fall? | Trade bonds | Buy “Fed cuts rates” |

| Will conflict escalate? | Trade FX or equities | Buy “Trade conflict escalates” |

Higher convexity, less capital

Another major difference between traditional global event hedges and the prediction market alternative is capital efficiency. Bond trades require a lot of capital, because price moves are relatively small. This is called “low convexity,” which means the payoff doesn’t accelerate much as you get closer to being right.

Prediction markets are the opposite. Since they’re tied entirely to a single outcome, the payoff increases much faster as you get closer to being right, so you need far less capital to express the same view.

Take a Fed rate cut example:

- Using bonds: A 25bps move might only shift prices by 1–2%. To hedge around $1M in potential losses, you may need a $50M–$100M position.

- Using a prediction market: If a “Fed cuts rates by 25bps” contract is trading at $0.40 (a 40% probability), you could target a similar $1M payout with only $670K. If the cut happens, it settles at $1 per contract and returns roughly $1M. If not, it goes to 0.

If a firm can’t deploy eight or nine figures through indirect exposure, they can take an infinitely smaller, more concentrated position tied directly to the outcome.

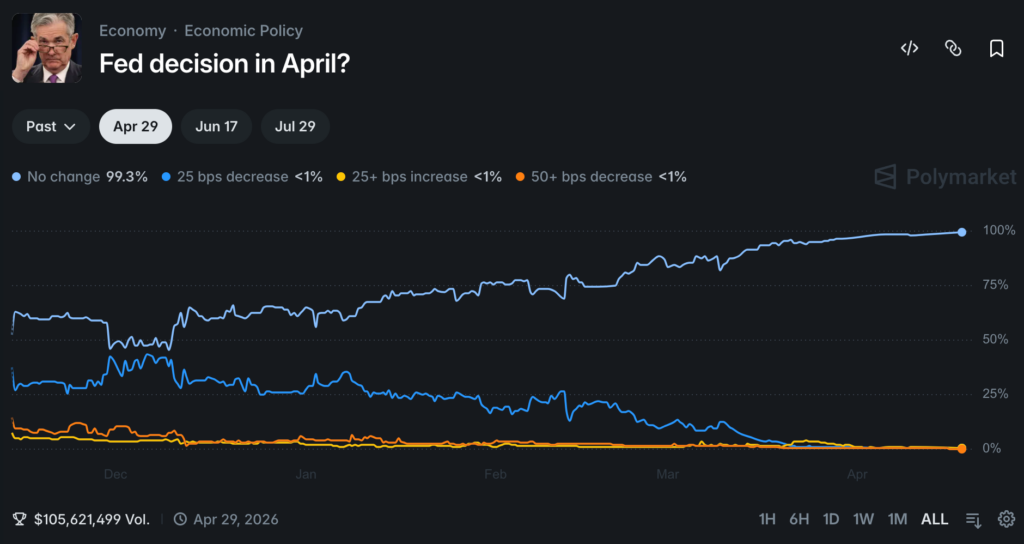

As we can see, this type of strategy may already be quite popular. The Fed decision market on Polymarket for April 2026 has seen more than $128 million in contract trading volume so far.

Inflation prints and jobs data

Another clear use case for prediction markets is economic data releases, not just for traders, but for businesses exposed to what these numbers drive. Inflation and jobs data can move interest rates, wages, consumer demand, and currencies. For a real estate firm, retailer, or logistics company, a single release can shift costs and margins overnight. A hot CPI print (consumer price index) can push rates higher and raise borrowing costs, while strong jobs data can push wages up and squeeze margins.

Traditionally, firms hedge this indirectly through rates, bonds, or FX. Again, prediction markets let you trade the outcome itself. Markets like “CPI above expectations” or “NFP below X” provide simple, event-level exposure.

Kalshi COO Luana Lopes Lara recently remarked that there were institutions participating in large block trades for “payroll hedging” on Kalshi, which industry observers speculate is likely referring to NFP (non-farm payrolls) data prediction markets.

These aren’t quite a perfect match for that use case, however, as NFP contracts track headline US labor data, not a company’s actual wage bill. As a result, the timing, structure, and payouts don’t cleanly align with how businesses experience those costs. So while the use case is directionally right, these markets still may not be a direct hedge for most participants.

Visible trading activity in these employment-related markets is still relatively modest, suggesting the markets are unlikely to fully explain the $20–30M block trades referenced. We’ve reached out to Kalshi for details of these trades and the avenues involved, but have not received a response at press time.

Regulation, elections, and policy risk

Regulatory and policy risk is one of the hardest things for businesses to manage. A single decision can wipe out revenue or add millions in costs overnight. Unlike typical markets, there’s no gradual move: a law either passes or it doesn’t, often with little warning. That makes them difficult to hedge using traditional tools. There are very few cases where assets give direct or approximate exposure to regulatory outcomes, so most companies rely on indirect signals or portfolio adjustments.

Yet again, prediction markets change that. A crypto company can hedge new regulation passing. A supplement brand can hedge restrictions being introduced. And a healthcare firm can hedge policy approvals. If there’s not way to trade around the impact, they can trade the outcome itself.

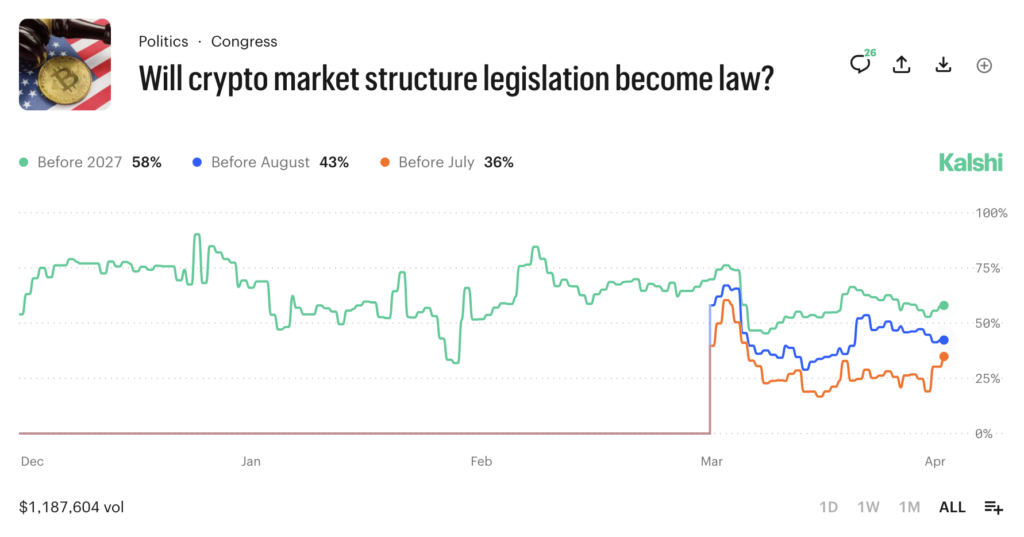

The recent CLARITY Act debate is a great example. Stablecoin issuers have been left in limbo over whether they’ll be able to offer yield on their tokens, with no clear way to manage that risk. Markets like Kalshi’s “Will crypto market structure legislation become law?” allow that uncertainty to be priced and traded directly (although liquidity is still limited for larger positions).

Kalshi CEO Tarek Mansour believes hedging on election prediction markets will gain momentum among institutions. “By mid-2027, having a position on the election will not be an unusual thing for an institution to have. And why? Because the alternative is pretty bad,” Mansour said at a recent Kalshi Research event.

“The demand to hedge on part or the other taking over is very clear, very well defined, and right now, people do it via proxies. And there is a better product now.”

Kalshi CEO on political hedging:

— Kalshi Research (@KalshiResearch) April 9, 2026

"By 2027, it will not be unusual for institutions to have a position on the election. Why? The alternative is pretty bad…People do it via proxies, but there's a better product now." pic.twitter.com/cnA06ujUgl

Prediction markets tend to work best in policy situations where:

- The outcome is binary, like a policy either passing or failing

- The timing is uncertain

- The financial impact is meaningful if things go the wrong way.

It’s also a gap traditional insurance simply doesn’t cover. You can’t easily buy a policy that pays out if a law passes or regulation changes your industry overnight. Prediction markets turn that uncertainty into something that can be priced and hedged in advance.

Event cancellations and revenue shocks

For event-driven businesses, revenue can disappear overnight. Many businesses are exposed to specific events that can sharply impact sales, but they’ve historically had limited ways to manage that risk. A cancellation, poor turnout, or unexpected disruption can wipe out a large share of expected revenue for a given period.

Take a bar during a major tournament. If the home team is knocked out, foot traffic can drop immediately. Or consider a ticketing company or event organiser. If an event underperforms or gets cancelled, the financial impact is instant.

A real-life example is the recent Wireless Festival cancellation in London, UK. When Kanye West was barred from entering the UK, the entire event was called off, wiping out over £30M in revenue almost overnight. While event insurance may cover parts of this, situations like this often fall into grey areas, where payouts are uncertain and depend heavily on policy wording.

That’s the current gap: Even when insurance exists, it can be slow, conditional, and not always reliable.

Prediction markets open the door for businesses to hedge things like weather cancellations through climate contracts. They also allow businesses to take positions on the event itself, instead of relying on coverage after the fact. If the event goes against them, the payout helps offset the loss.

Markets have already emerged around whether Kanye West will be allowed to perform in other countries, reflecting real-time uncertainty as France considers banning him from performing in Marseille on June 11.

In effect, prediction markets give businesses flexibility to create their own DIY insurance, tailored to the risks they actually face. For companies with uneven, event-driven revenue, that provides a more direct way to manage downside.

Sportsbook exposure and team performance risk

Sports is an area primarily associated with speculative trading, but it’s also where prediction markets are moving beyond into real risk management use cases. At a basic level, sportsbooks and insurers take on risk. If too many customers bet one side, or if a team hits a milestone like making the playoffs or triggering a bonus, they can face large payouts.

Traditionally, that risk gets offloaded through reinsurance. But that process is slow, opaque, and negotiated privately. Here’s how prediction markets can play a role:

- A sportsbook with heavy exposure on one team can hedge by buying “Team A wins” contracts.

- If the team wins and payouts spike, the market position offsets the loss. If not, the hedge expires and they keep the upside.

Insurers can do the same. If they’re exposed to performance bonuses, like a team making the playoffs, they can buy contracts tied to that outcome and offset the risk directly.

This is already starting to happen. Last February, Kalshi partnered with Game Point Capital, a firm that issues hundreds of millions in sports insurance annually. Some of that exposure is already being hedged on-platform, with Mansour highlighting some significant pricing differences:

- “Team makes playoffs” hedges priced at around 6% on Kalshi vs 12–13% OTC

- “Team advances to second round” priced at about 2% vs 7–8% OTC.

That pricing gap is significant, reflecting a shift from private, negotiated risk transfer to open, market-based pricing.

Liquidity is also improving. During the Super Bowl, Kalshi reportedly had the liquidity to handle a $22M trade without major price impact. Their head-to-head market alone saw over $500M in notional trading volume, with Polymarket exceeding $700M on their NFL champion market.

Kalshi is also actively incentivising this flow. At around the same time it partnered with Game Point Capital, it also filed with the CFTC for a Sportsbook Hedging Rebate Program. This proposed to offer 100% fee rebates on large trades (300k+ contracts) to attract institutional users.

There are still open questions around adoption of these two initiatives, however, particularly about how much of this flow is actually coming from sportsbooks and insurers.

But if it scales, the implications are clear. Rather than relying on reinsurance or holding risk internally, firms can offload exposure into a liquid, competitive market.

We’ve reached out to Kalshi for the current status of both initiatives, but have not received a response as of yet.

Weather, temperature and demand shocks

Many of the use cases above already overlap with insurance, but one specific type is especially relevant here: parametric insurance. Parametric insurance is insurance that pays out automatically when a predefined event occurs. You don’t need to prove damages or losses; if the trigger is met, you get paid, no questions asked.

For example, if rainfall drops below a certain level or temperatures exceed a threshold, the contract pays out immediately, regardless of the actual damage. That makes it faster and simpler than traditional insurance, but less precise, since payouts don’t always match up to real-world losses.

Pompliano mentioned this use case in a recent X post about the utility of prediction markets for capital allocation and hedging. “An obvious use case for these types of markets would be farmers who are looking to leverage prediction markets as a replacement for their current hedging or insurance strategies.” Kalshi has also recently expanded its commodities market offerings.

Trade on more commodities.

— Kalshi (@Kalshi) April 15, 2026

24/7.

Now on Kalshi. pic.twitter.com/0IugqAk9eD

There are already signs this type of contract is being used at scale in real-world settings. As Interactive Brokers Founder and Chairman, Thomas Peterffy, noted in a recent earnings call:

“Our most frequently traded [prediction market] contracts are temperature contracts…utilities have to every day make a judgment about the next use of electricity.”

This is parametric insurance via prediction markets, already in practice before our eyes. Utilities are exposed to weather and energy demand, and temperature-based contracts allow them to hedge that risk directly. If temperatures move beyond a certain level, the contract pays out immediately.

This overlaps with areas like weather derivatives and disaster hedging, but expands access far beyond traditional players. They’re open and flexible markets, which are priced in real time rather than negotiated through insurers.

Deploying capital at institutional scale

All of the use cases so far rely on one key assumption: That institutions can actually deploy meaningful capital into these markets. That’s the next hurdle, and it will depend on infrastructure and liquidity catching up to institutional needs.

Obviously it’s one thing to have a view on rates, inflation, or geopolitics. It’s an entirely different thing to put millions of dollars behind that view, without moving the market against yourself.

Citadel Securities is already circling this bottleneck. As one of the world’s largest market makers, its role wouldn’t just be participation, but providing the liquidity needed for institutional size.

The case for prediction market block trading

In traditional finance, this is handled through tools like block trading. Block trades let large players enter positions with minimal market impact, often by matching large orders directly instead of relying on the public order book.

For prediction markets to become a true institutional tool, they need to offer something similar, and there are early signs this may be happening. As touched on earlier, Kalshi COO Luana Lopes Lara has said block trades are already live, with deals already occurring in the $20–30M range. If that’s accurate, it suggests prediction markets are starting to handle institutional-sized positions, which could very well open the floodgates to more major participation.

But it’s still early. There’s very little public visibility into trades of that size, and no clear documentation around how block execution actually works on DCMs. That’s what makes this stage interesting.

If prediction markets can support large, discreet trades with enough liquidity and minimal price impact, they open the door to a much broader set of users, from macro funds and insurers to businesses managing real-world risk.

Once that happens, prediction markets won’t be known as platforms “just for betting” anymore. They might just become the go-to option for pricing and hedging real-world risk.

From indirect exposure to direct outcomes

Prediction markets are still early, but the direction is becoming hard to ignore. Right now, they still sit somewhere between speculation and real financial infrastructure. Institutions are testing them, probing where they work, and taking advantage of pricing gaps while they still exist.

But as liquidity improves and execution matches it, prediction markets will likely find their place alongside traditional financial tools as part of serious investment and risk management strategies.

Whether its elections, economic data prints, supply chains, regulation, demand, or geopolitical events, institutions no longer have to wait to react to those events after they’ve happened. If they need to, they can start pricing those outcomes continuously and positioning ahead of them with precision.

Once that plays out, prediction markets won’t be a niche tool anymore; they’ll be sitting right next to your Bloomberg terminal.