Thursday’s closed-door GOP crypto market structure meeting signaled progress is being made on a compromise on stablecoin yield; however, conversations remain in a “delicate state,” crypto journalist Eleanor Terrett reported on Twitter.

Senator Cynthia Lummis’s press team highlighted that discussions surrounding stablecoin yield are “99% of the way there,” while negotiations on the digital asset portions of the bill are “in a good place.”

The breakthrough, if reached, would mark a significant step forward for lawmakers working to finalize the Clarity Act.

But even as a compromise comes into view, the debate over yield has exposed a deeper and still unresolved question in the midst of US crypto policy. Should stablecoins function purely as payment instruments, or evolve into yield-bearing financial products that begin to resemble bank deposits or money market funds?

If stablecoin issuers can offer yield, what should that yield be considered (legally)?

At the center of the stablecoin debate lies an important question: if stablecoin issuers can offer yield, what should that yield be legally considered?

Essentially, this also encompasses one of the biggest power dynamics dominating financial markets today, at least in the United States: Wall Street vs Crypto.

Speaking with DeFi Rate, the CEO of Borderless.xyz, a global best-execution orchestration network for stablecoin on and off-ramps, Kevin Lehtiniitty, explained that if stablecoin providers were to offer yield, that yield, in the eyes of traditional financial players, would be considered “interest.”

“Tokenization does not change that [definition]. Calling it rewards or staking doesn’t really hold up, and you have to look at what’s happening to the underlying dollars,” Lehtiniitty said.

Rodrigo Coelho, CEO of Edge & Node, echoed that concern, noting that if yield is treated as interest, it would effectively create a deposit product, making stablecoin issues “subject to banking rules they’re not built for.”

“The Senate draft tries to split the difference by banning yield on idle balances but leaving room for activity-based rewards. The problem is the line between those two things is blurry enough to be gamed in both directions.”

However, that ambiguity has also opened the door to competing interpretations across the industry.

Ethan Buchman, co-founder and CEO of Cycles, argued that stablecoin yield should not be forced into existing regulatory categories at all, but instead treated as part of a new framework aligned with “narrow banking” principles. In this model, yield generated from government debt could be passed through to users without transforming issuers into full-service banks.

The lines between crypto and TradFi are blurring

If the debate surrounding stablecoin yield is resolved, experts are predicting that the distinction between traditional finance (TradFi) and crypto will start to blur even further.

Edge & Node’s Coelho noted that if stablecoin issuers are allowed to issue yield, they would become something akin to a “bank without the charter, capital requirements, or deposit insurance.”

“That’s what the banking lobby is afraid of, and they’re not entirely wrong. But it cuts both ways.”

Banks are already moving into stablecoins with SoFi’s launch of SoFiUSD and JPMorgan putting JPMD on Base.

For some industry participants, allowing stablecoin issuers to offer yield would effectively push them into bank-like territory.

“You are taking retail deposits, investing them, and paying a return … you have replicated the core function of a bank,” Lehtiniitty said, adding that this would place issuers closer to money market funds or deposit-taking institutions in practice.

Others argue that this evolution is not only inevitable but desirable. Jamie Green, COO of Superset, described yield-bearing stablecoins as a form of “narrow banking,” where deposits are fully backed by high-quality liquid assets, and returns are passed directly to users. Unlike traditional banks, he noted, these models do not rely on leveraged lending or maturity transformation, features that have historically introduced systemic risk.

“The banking lobby is framing this as a consumer protection issue, but what they’re actually saying is: we don’t want to compete with a simpler, more transparent model that doesn’t need a taxpayer-funded backstop to survive.”

The prospect of stablecoin issuers competing for deposits, without being subject to the same capital requirements, liquidity rules, or deposit insurance frameworks, has intensified lobbying efforts from the banking sector.

What can we expect next?

Superset’s Green noted that the existing prohibition language on issuer-paid yield is “essentially dead in its current form,” with negotiators now exploring either permitting yield under strict conditions or tightening definitions to close potential loopholes around platform-distributed rewards.

Those definitions, particularly around what constitutes a “payment stablecoin” or an “inducement,” are emerging as some of the most contested elements of the bill. As Green explained, the current language is “drafted loosely enough that clever counsel can structure around any restriction,” raising concerns that the legislation could be undermined in practice if not carefully refined.

Others expect changes to extend beyond yield itself. Edge & Node’s Coelho highlighted that definitions around permitted payment stablecoins and the scope of services providers can offer are already being revisited, while also pointing to ongoing disagreements over anti-money laundering (AML) requirements for decentralized protocols.

Reserve composition rules are another area under scrutiny. Jimmy Xue, the COO and co-founder of Axis, argued that what issuers are allowed to hold as backing assets will ultimately determine which yield strategies are viable, warning that the current scope is “far too narrow” to support the competitive market.

Shifting Clarity Act timeline and odds

As for the April deadline that Senators have brought up in conversations, industry experts remain skeptical following past delays.

“The White House’s March 1 deadline evaporated. Banking Committee hasn’t completed markup. Even if Alsobrooks gets a late-March markup done, you still need reconciliation with the Agriculture Committee version, floor debate, House passage, and conference,” Green said.

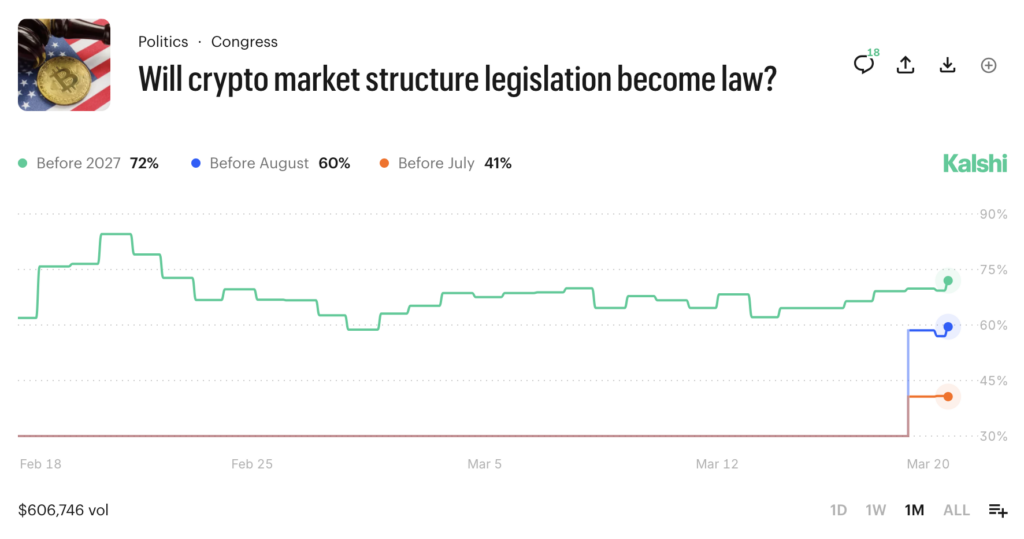

Polymarket odds place the Clarity Act being signed into law in 2026 at 63% as of the time of writing, which, according to Green, is an indication we could see this happen, “but not remotely on the current timeline.”

Kalshi traders are a bit more optimistic, putting the odds at 72% crypto market structure legislation will become law by the end of the year.