On the surface, Opinion Lab’s upstart onchain prediction market is a historical growth story and an unlikely candidate to rival Kalshi and Polymarket for top exchange status. But it raises an obvious question: Is Opinion’s growth real?

The BNB Chain-native prediction market launched its mainnet on Oct. 23, 2025, cracked $1 billion in weekly volume within a month, and by December was posting more notional volume than either Kalshi or Polymarket. In January, Opinion.Trade generated $8.08 billion in monthly notional volume — roughly 31% of the entire tracked prediction markets industry’s output. A Hong Kong-based startup, backed by Binance founder Changpeng “CZ” Zhao‘s venture arm, had outpaced two well-funded, years-old exchanges within weeks of going live. It’s the fastest platform ascent in prediction market history.

But there’s another story in the same data. Throughout Opinion’s run, a set of persistent anomalies have separated it from every other prediction market platform we track: trade sizes 13–25x larger than competitors, a user base that swings 6x in a matter of weeks, and a volume-per-user figure that doubled as the platform scaled, the opposite of what organic growth typically produces. We dug into the data from Dune to explore what’s behind Opinion’s rapid ascent, and what to make of it.

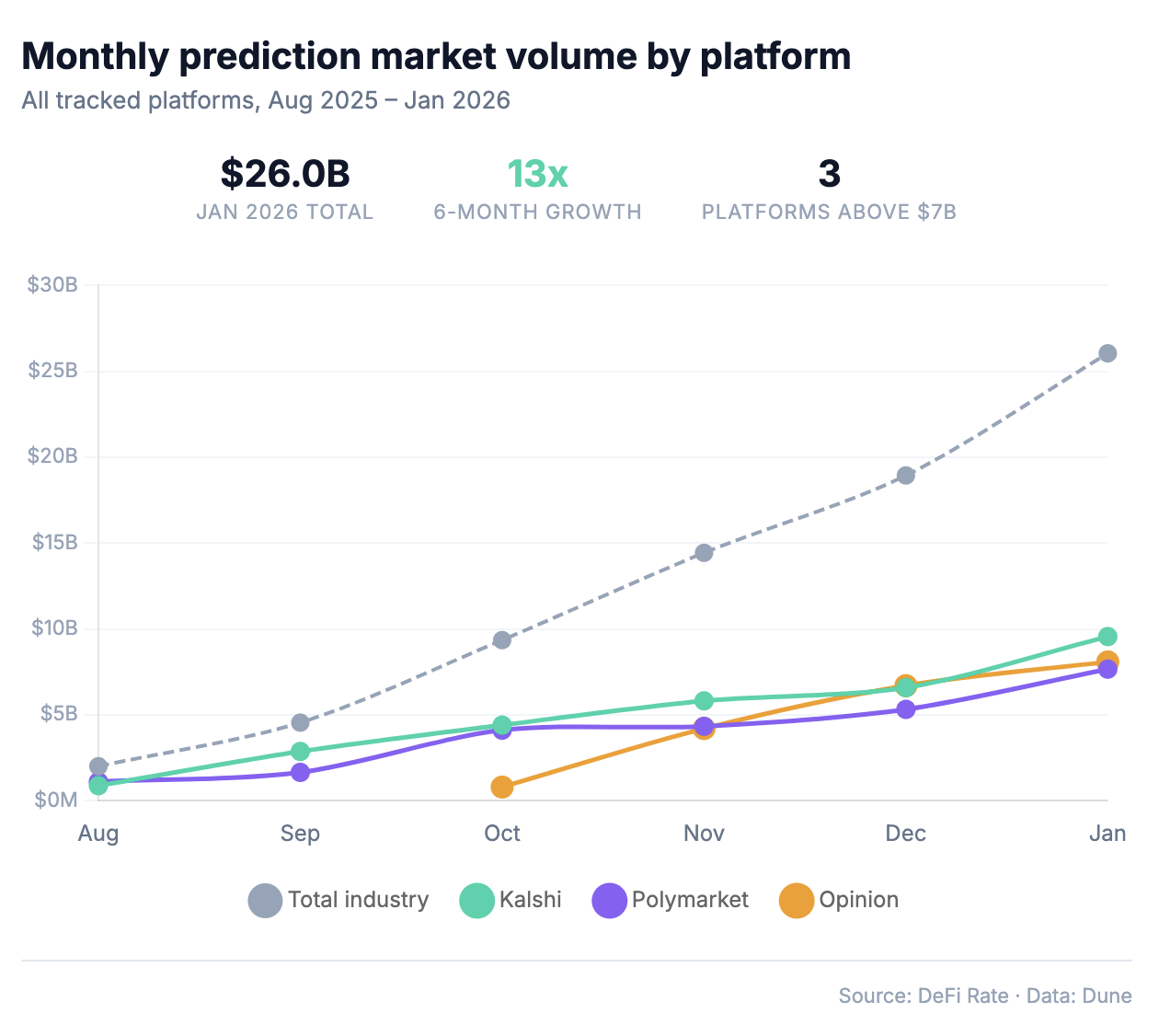

Industry growth context: $2 billion to $26 billion in six months

The industry-level growth is staggering and real. As we reported in a recent volume report, the prediction market industry grew roughly 13x in six months, from $2 billion in total monthly volume in August 2025 to $26 billion in January 2026. That growth was not evenly distributed, and Opinion’s arrival was a major part of the story.

Kalshi’s monthly volume went from $874 million (Aug) to $9.55 billion (Jan), an 11x increase driven overwhelmingly by sports. Polymarket grew from $1.1 billion to $7.66 billion, a 7x increase, with a more diversified split across sports, crypto, and politics. Both trajectories reflect sustained growth over six months driven largely by sports markets including NFL trading interest, and a steady stream of partnerships and new distribution channels.

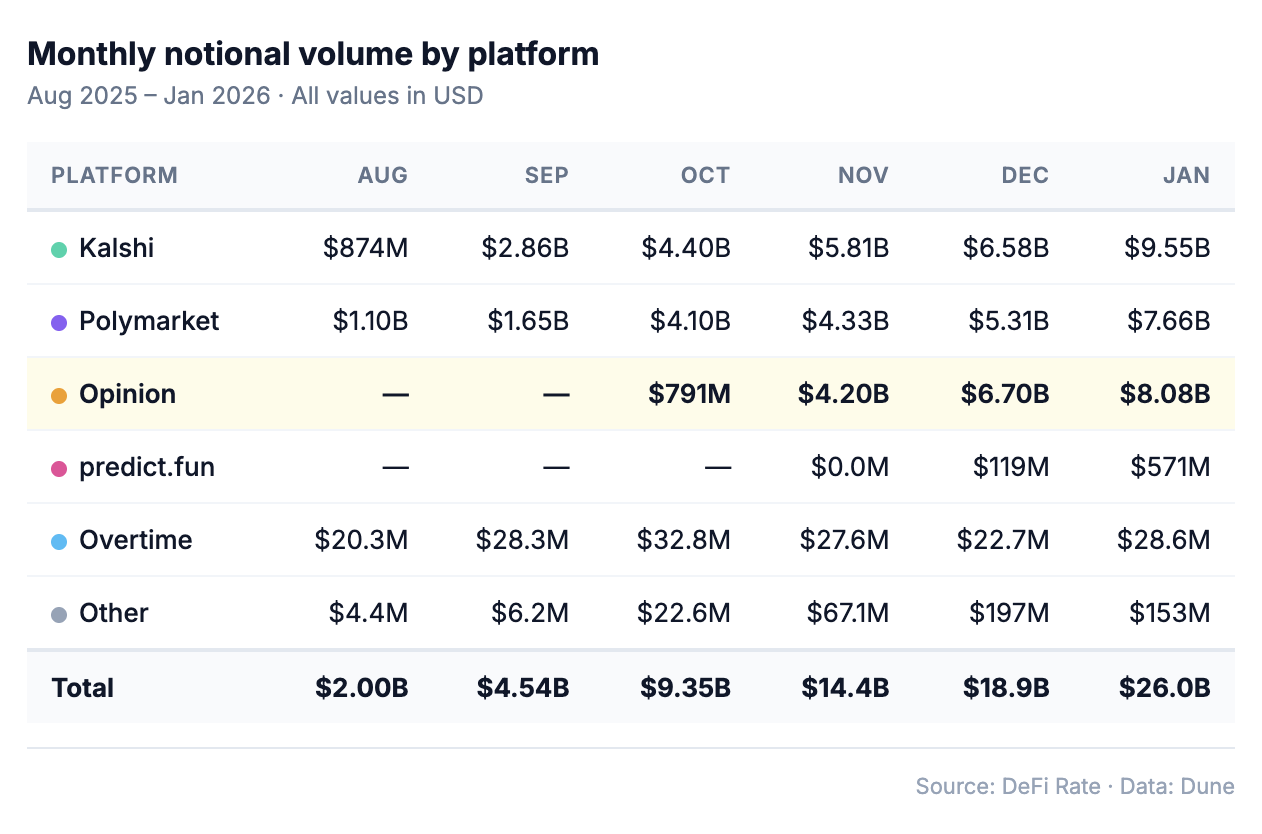

Opinion didn’t exist in August or September. It launched Oct. 23, posted $791 million in its first partial month, hit $4.2 billion in November, and by December was generating $6.7 billion — more than either Kalshi or Polymarket that month. No prediction market platform has ever scaled that fast.

That rapid ascent drew immediate attention. Within weeks of launch, CryptoTimes documented X users noting “decreasing transactions while increasing volume” and “10x volume volatility day over day,” calling it “obvious volume manipulation, similar to Aster DEX.” CoinLaw’s coverage around the same period noted the growth was “maybe too explosive” and flagged the Aster comparison, a reference to the YZi-backed perpetual futures exchange that exhibited similar volume patterns on BNB Chain.

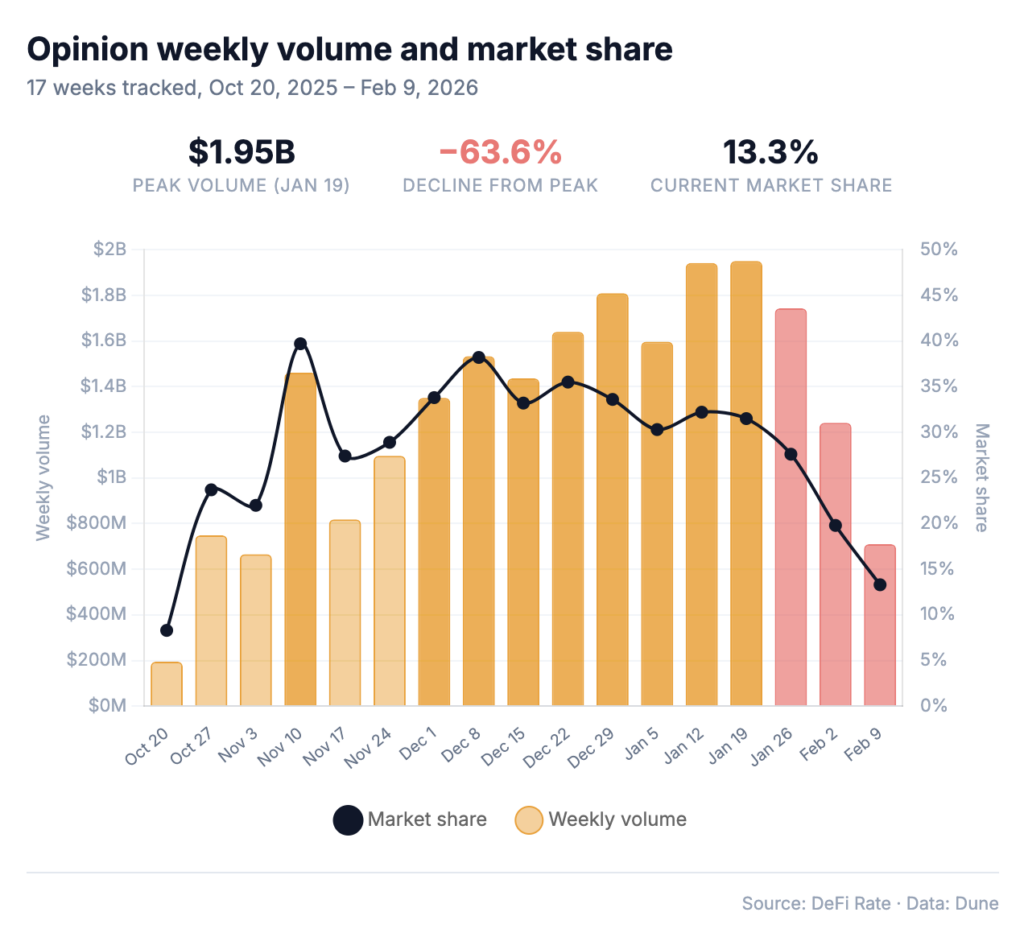

Those early flags didn’t slow Opinion’s growth. Its volume kept climbing into the new year, peaking at $1.95 billion the week of Jan. 19. Then its recent decline began. And the data the early observers flagged has only intensified.

What the weekly data actually shows

Dune has tracked Opinion weekly since Oct. 20. The full 17-week dataset tells the story in sharper resolution than the monthly figures. Note: This report includes Dune data through Feb. 15, 2026.

Opinion held the #1 global volume position for three separate weeks: Nov. 10 ($1.46B), Dec. 1 ($1.35B), and Dec. 8 ($1.53B). During the week of Nov. 10, it produced 53% more volume than Polymarket despite processing 19x fewer transactions. Its peak weekly volume was $1.95 billion (Jan. 19), at which point it held a 31.5% share of the entire industry.

Then it fell. Four consecutive down weeks: $1.95B → $1.74B → $1.24B → $709.7M. That’s a 63.6% decline, by far the steepest pullback of any major platform during that stretch. As we noted in our Feb. 9 volume report, “Opinion’s 28.7% WoW drop to $1.24 billion is its lowest weekly volume since early January and pushes it firmly into third, well behind the Kalshi-Polymarket pair.” The following week it dropped another 42.8%.

To put the volatility in perspective: Kalshi dipped 13.2% from its recent high over the same four-week period. Polymarket fell 1.9%. Opinion fell 63.6%. As we’ve written previously, Opinion “swings harder in both directions than its larger competitors.” That pattern has been visible throughout its life: week-over-week changes of +283%, −11%, +119%, −44%, +34%, and so on. No other tracked platform exhibits anything close to this level of volatility.

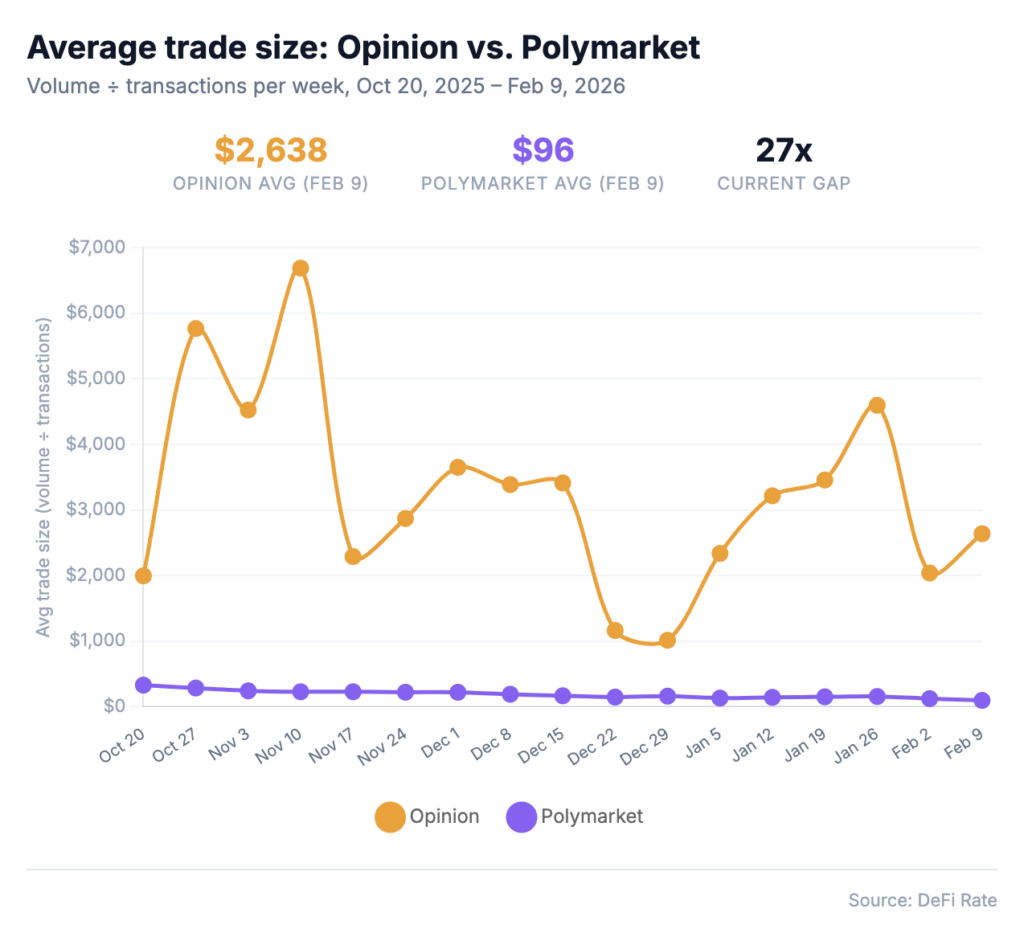

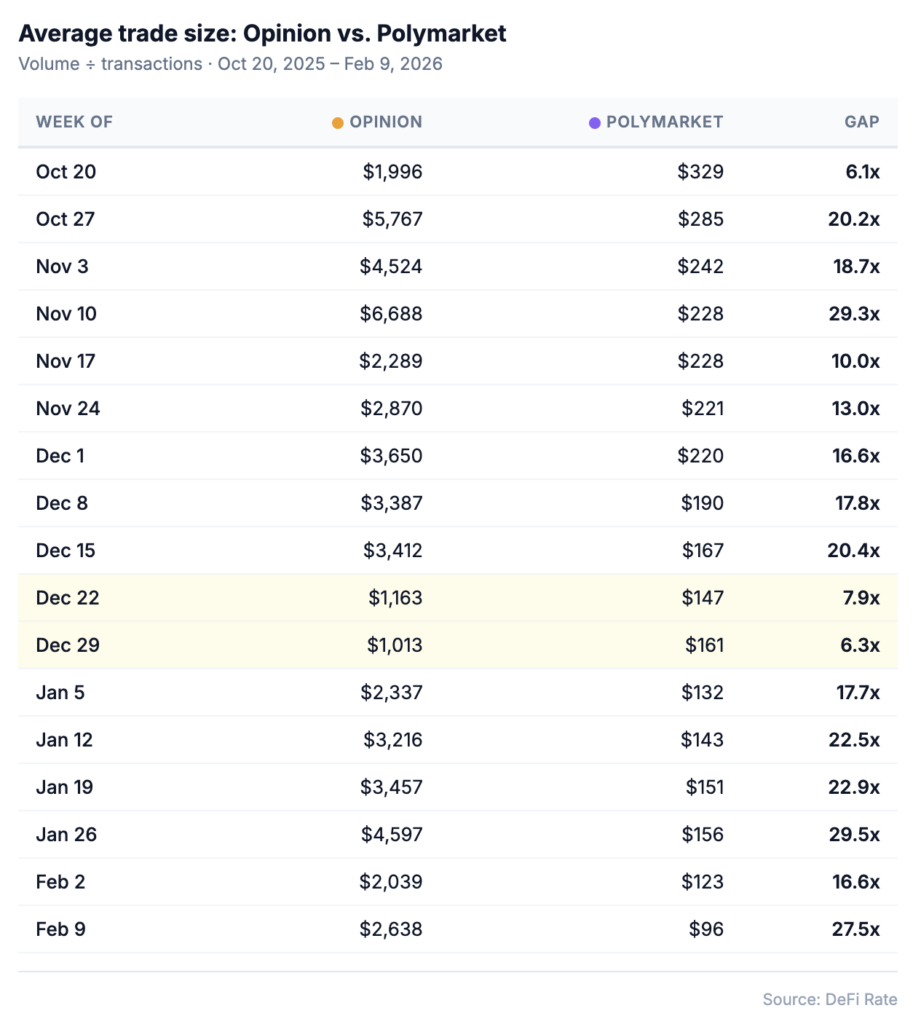

The trade-size anomaly: Opinion’s defining data point

While volume is the headline number, transactions tell a different story. In January 2026, Opinion generated $8.08 billion in volume from 3.2 million transactions for an average trade size of roughly $2,525. That same month, Kalshi generated $9.55 billion from 54.5 million transactions ($175 average). Polymarket generated $7.66 billion from 52.0 million transactions ($147 average).

Opinion produced 31% of January’s industry volume from less than 3% of its transactions.

This has been the platform’s structural signature since launch. As we reported in our post-Super Bowl volume report: “Opinion’s 608,906 transactions against $1.24 billion in volume continues to underscore its unusually large average trade size of roughly $2,038 per transaction, compared to $157 at Kalshi and $123 at Polymarket.”

Across the first 17 weeks of Dune tracking, Opinion’s average trade size has ranged from $1,013 to $6,688. Polymarket’s range over the same period is $96–$329 with a steady and consistent downward trend as the platform adds more retail users. Opinion’s trade size has never once converged toward industry norms.

The week of Nov. 10 was the starkest illustration. Opinion posted $1.46 billion in volume from 218,582 transactions ($6,688 average). Polymarket posted $952 million from 4.19 million transactions ($228 average). That was 19 times fewer trades and 53% more volume.

There’s one notable exception over the Dec. 22–Jan. 4 holiday period. During those two weeks, Opinion’s transactions surged to 1.4–1.8 million (from a typical 300K–600K), and its average trade size dropped to the $1,000–$1,163 range. This was the only period where Opinion’s activity profile looked more like a normal prediction market. Then it snapped back. One possible interpretation: genuine retail participation surged during the holidays, possibly from a promotional push, temporarily diluting the platform’s whale and farming base, then receded as those users moved on. Or maybe something else.

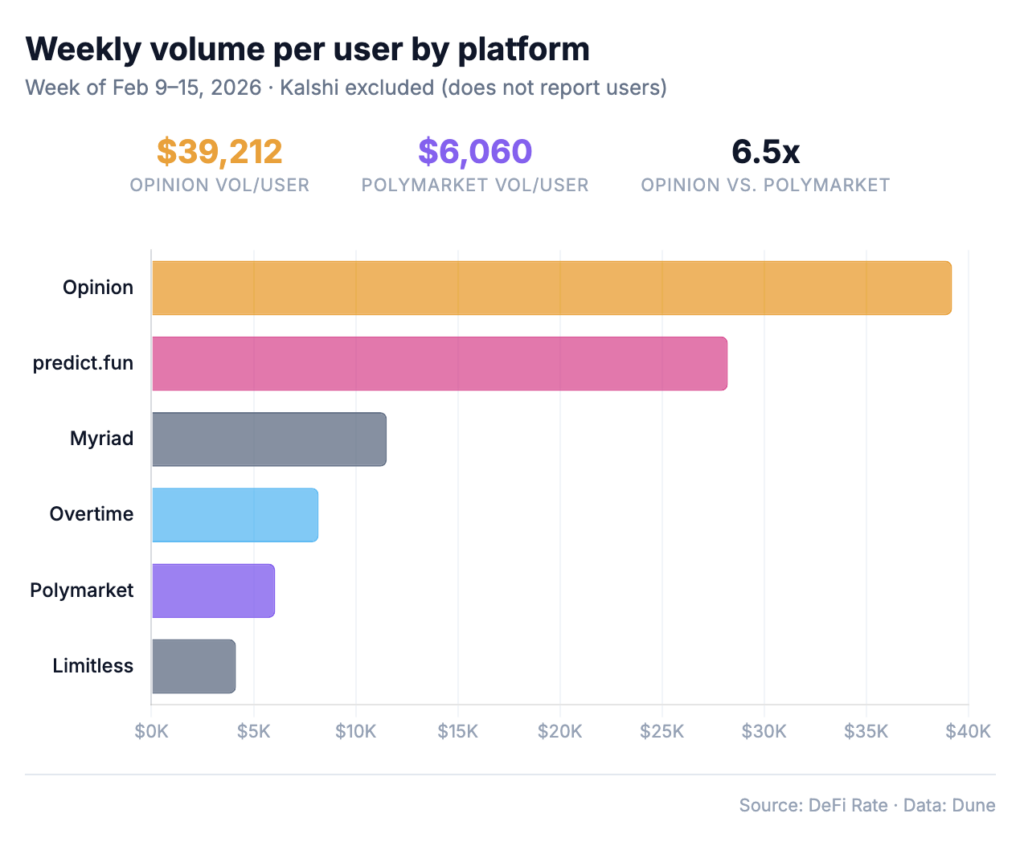

Volume per user: Where the gap is widest

The per-user figures amplify everything. For the most recent tracked week (Feb. 9), Opinion had 18,098 weekly active users generating $709.7 million, roughly $39,200 per user. Polymarket’s 309,991 users generated $1.88 billion, about $6,060 per user. The gap is 6.5x.

What’s more unusual is the trajectory. The monthly data shows Opinion’s volume per user doubled as the platform scaled, from $38,537/user in October (20,534 users) to $79,241/user in January (101,954 users). Normally, growing a user base 5x dilutes per-user metrics as new, more casual users join. On Opinion, each successive cohort traded more aggressively than the last. That’s the opposite of what organic growth typically produces on platforms like Polymarket, where per-user volume has grown steadily but gradually ($4,852/user in August to $11,817/user in January — a 2.4x increase with 2.9x more users).

The user base itself is remarkably volatile, another potential red flag. Total users have swung from 11,124 (launch week) to 67,913 (Dec. 29) and back to 18,098 (Feb. 9). Two distinct spikes came during the Dec. 22–Jan. 4 holiday period (66K–68K users) and the week of Feb. 2 (67,804). Both were followed by sharp contractions. The Feb. 2 to Feb. 9 drop (67,804 to 18,098), a 73% decline in one week, was the most dramatic user swing of any platform in our dataset.

Polymarket’s user base, by contrast, has ranged from 214,962 to 323,525 over the same 17-week period, a 1.5x range with a steady upward trend.

What’s driving the numbers: The points system

There are some potential explanations for the data anomalies, including a specific incentive design.

Opinion runs the OPINION Point System (PTS), its primary mechanism for rewarding participation ahead of an expected token launch ($OPN). Per the platform’s official documentation, a fixed pool of 100,000 points is distributed weekly to users who meet a $200 minimum volume threshold. Points are scored across three dimensions: limit order placement (rewarding liquidity provision near the market mid-price), trade size (explicitly “designed to reward conviction and information contribution”), and position holding duration.

There is no token yet, and no fixed conversion rate. Essentially, users are farming for an airdrop with speculative upside. Multiple third-party guides walk users through the optimization: Whales Market instructs users to “provide liquidity, trade with quality, hold your positions.” CoinLaunch describes it as “soft airdrop farming with extra steps.”

The points structure creates several dynamics that help explain the volume patterns. The $200 weekly minimum ensures every active user generates at least that much in “motivated” volume. Larger trades earn proportionally more points, which directly incentivizes the outsized trade sizes we’re seeing. And then position holding inflates open interest as a secondary metric. And the pre-token environment means all of this activity likely skews toward speculative trading rather than expressive of genuine market views.

None of this is unique to crypto. But the combination of a pre-token airdrop, explicit rewards for larger trades, and a no-KYC environment creates a powerful set of incentives that may help explain the magnitude of the anomalies.

Right on Dune’s data dashboards reads the following disclaimer: “There is no filter for wash volume applied currently so be cautious.” All signs point to wash volume being a major factor in Opinion’s tracked volume figures.

Wash trading: The Polymarket precedent

Incentive-driven volume isn’t new. In fact, academic and industry research has documented incentive-driven volume inflation on the largest onchain prediction market.

In November 2025, Columbia University researchers estimated that roughly 25% of all Polymarket trading volume over three years was likely generated by “wash trading,” where users engage in artificial, circular, or self-dealing transactions to create the illusion of higher activity. Sports markets were hardest hit at 45% of all-time sports volume. The researchers flagged 14% of the platform’s 1.26 million wallets for suspicious activity consistent with wash trading, such as repeatedly buying and selling the same contracts in a short period. The findings indicate that this practice significantly inflates the platform’s volume metrics, particularly around speculation for potential token airdrops.

The structural factors the Columbia researchers identified — no KYC, pseudonymous accounts, no trading fees, and a potential future token — overlap substantially with Opinion’s model. One significant difference: Opinion does charge trading fees, which adds friction that Polymarket’s zero-fee environment lacked. But Opinion’s active PTS system, with its explicit rewards for larger trades, adds an additional incentive that Polymarket’s setup didn’t have.

| Factor | Kalshi | Polymarket (Global) | Opinion |

|---|---|---|---|

| CFTC regulated | Yes (DCM) | Yes (via QCX) | No |

| KYC required | Yes | Partial | No |

| Trading fees | Yes | Zero | Yes |

| Token launched | N/A | No | No (PTS active) |

| Avg trade size (Feb 9) | ~$135 | $96 | $2,638 |

| Vol per user (Feb 9) | N/A | $6,060/wk | $39,212/wk |

| Independent wash trading study | N/A | Yes (25-33%) | None published |

No independent analysis of Opinion’s on-chain volume integrity has been published, at least as of yet. But the data is available on BNB Chain. Opinion has not returned our requests for comment.

Key takeaways from Opinion trade data analysis

Here’s what 17 weeks of Dune data, six months of monthly figures, and our own weekly volume tracking tell us in aggregate:

The volume is real, in the sense that it happened onchain. Opinion generated massive trading activity on BNB Chain. At its January peak, 101,954 monthly users produced $8.08 billion in volume. It’s a functioning prediction exchange with working infrastructure and market resolution.

But the volume-to-transaction ratio has never looked normal. Opinion’s share of industry transactions peaked at 8.6% (Dec. 29) even as its volume share hit 33.6%. By Feb. 9, it was generating 13.2% of industry volume from roughly 0.7% of industry transactions — a 19:1 ratio that no other platform approaches. That gap has been consistent since launch.

The user base volatility is unmatched. Swings from 11,124 to 67,913 and back to 18,098 suggest campaign-driven activity cycles, not organic growth. Polymarket’s user base varies 1.5x. Opinion’s varies 6x.

The volume-per-user ratio grew as the platform scaled, not shrunk. From $38,537/user in October to $79,241/user in January. In normal platform growth, new users dilute the average. On Opinion, each successive cohort traded larger.

The holiday anomaly is telling. During Dec. 22–Jan. 4, transactions surged, average trade size dropped to ~$1,000, and the user base hit 66K–68K. It was the only period where Opinion’s data profile resembled a typical prediction market. But then it reverted.

These patterns are consistent with incentive-driven activity: airdrop farming, points optimization, and inflated trading volumes. They’re also consistent, at least in theory, with a genuinely institutional user base making large macro bets. The difference between those two explanations matters for Opinion’s valuation, for how the industry counts growth, and for the credibility of volume as the metric by which prediction markets are compared.

Where things stand now

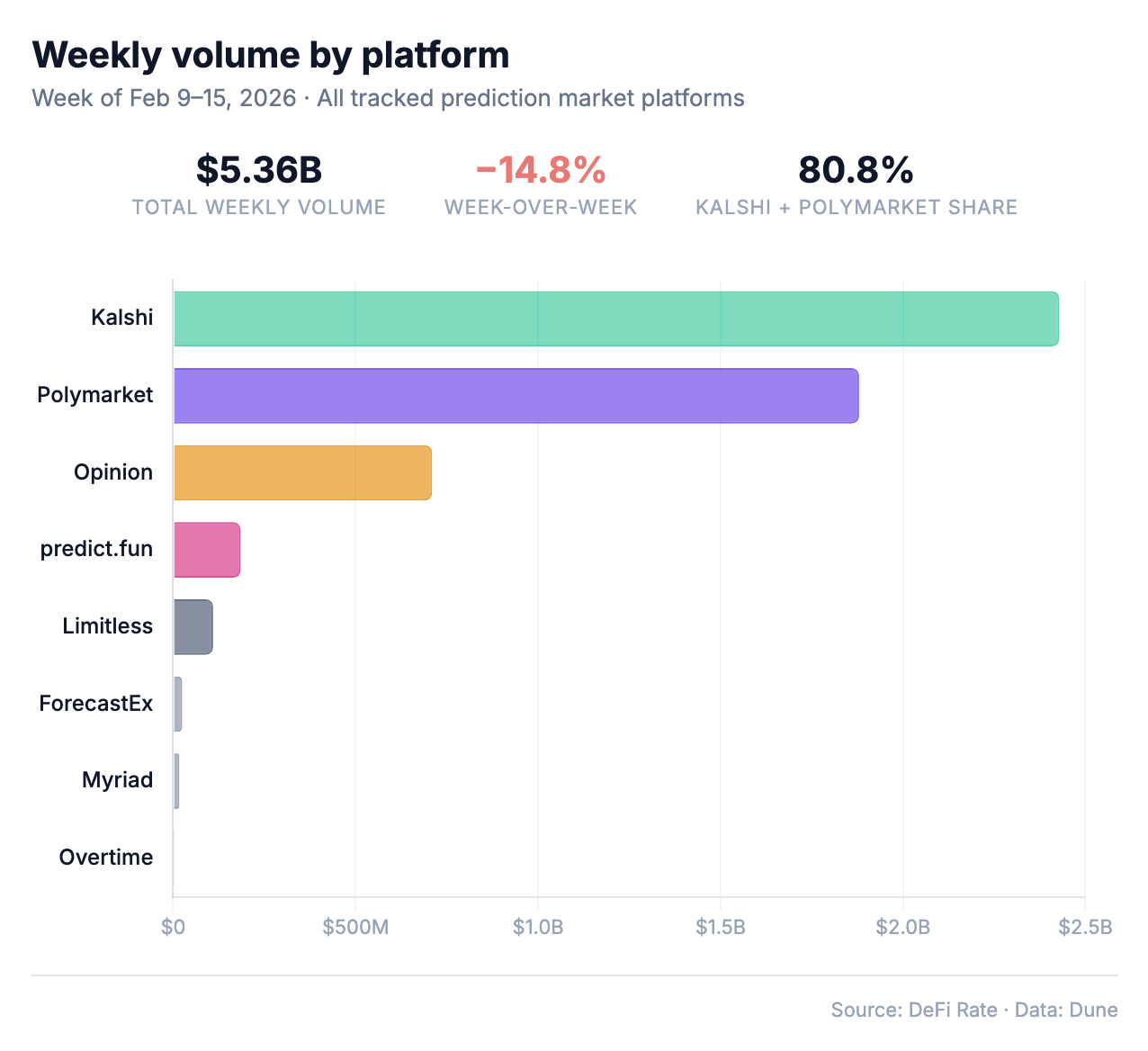

Opinion remains the third-largest prediction market platform at $709.7 million weekly, comfortably ahead of predict.fun ($184.7M), Limitless ($109.4M), and the rest of the field. It has real infrastructure, credible institutional investors (Hack VC, Jump Crypto), and market offerings, including macro events, crypto/TGE outcomes, and esports that fill genuine gaps in the Kalshi/Polymarket landscape, particularly for non-U.S. traders who can’t access CFTC-regulated exchanges.

But the data we’ve compiled should give readers a framework for evaluating what those headline volume figures represent. An average trade size 27x larger than Polymarket’s, a user base that swings 6x in weeks, a volume-per-user figure that doubled as the platform scaled, and an incentive system that explicitly rewards larger trades are all data points that warrant scrutiny, the same kind of scrutiny that Columbia’s researchers and other like Chaos Labs have applied to Polymarket.

The methodology exists and the on-chain data is public. But in-depth analysis hasn’t been done. Until it is, Opinion’s volume numbers are what they are: large, likely inflated, and open to interpretation.

Volume, transaction, and user data sourced from Dune Analytics prediction market dashboards. Kalshi and Polymarket real-time data from DeFi Rate’s prediction market tracker. Historical volume data compiled from DeFi Rate’s weekly volume report series.

Who’s behind Opinion Labs?

Before getting into the numbers, let’s look at the context around what Opinion is and where it came from, as the platform’s backing and regulatory positioning shape how its volume figures should be interpreted.

Opinion Labs was founded in 2023 in Hong Kong by Forrest Liu, a Columbia University graduate and former corporate finance associate at CMB International Capital (China Merchants Bank’s investment banking arm). A co-founder referenced as “KJ” appears in Messari’s December coverage as an expert in blockchain infrastructure, but there’s no public last name or background available. Beyond those two, the team is largely unidentified. CoinLaunch’s project analysis flagged that “there is limited information about core team members available.” There’s also no public team page on the Opinion website.

That’s not unusual in crypto. Bitcoin itself was created pseudonymously, and major DeFi protocols run with anonymous teams. But it does distinguish Opinion from the platforms it’s competing with for top-3 status. Kalshi’s leadership — CEO Tarek Mansour and COO Luana Lopes Lara — is extensively public and has testified before Congress. Polymarket’s Shayne Coplan has been profiled by the New York Times and appeared at the DealBook summit. For a platform handling billions in monthly volume and backed by $25 million in venture funding, the information gap is worth noting.

The more significant part of the backstory is the money behind it.

Who is bankrolling Opinion prediction exchange?

YZi Labs (formerly Binance Labs), CZ’s personal venture arm, led Opinion’s $5 million seed round in March 2025 alongside Animoca Ventures, Amber Group, Manifold Trading, and Echo. The platform launched exclusively on BNB Chain, making it the flagship prediction market for CZ’s blockchain. CZ confirmed the stake in a now-deleted X post, per crypto.news: “We are just a minority investor, but we try to help with adding strategic value.”

In February 2026, Opinion raised an additional $20 million in a pre-Series A led by Hack VC and Jump Crypto, reportedly at a valuation above $500 million.

But Opinion isn’t CZ’s only prediction market play. predict.fun, also on BNB Chain and also YZi-backed, was founded by a former Binance employee and introduced by CZ on X in December 2025. Also now tracked by Dune, predict.fun posted $571 million in notional volume in January. CZ’s Trust Wallet (220 million users) added prediction trading features in partnership with Polymarket, Kalshi and Myriad. YZi’s $1 billion Builder Fund targets DeFi and AI projects on BNB Chain. And crypto observers have drawn parallels to Aster DEX, another YZi-backed project that scaled rapidly on BNB Chain to rival Hyperliquid in perpetual futures volume, a comparison that will become relevant when we get to the data.

CZ appears to be diversifying in the prediction markets space, and has pushed back on winner-take-all framing. “This isn’t a ‘winner-takes-all race,'” he told crypto.news. “In any market, multiple players usually coexist.”

He credits Kalshi and Polymarket with mainstreaming the category and describes YZi’s approach as multi-platform, building BNB Chain’s share of the ecosystem rather than backing a single challenger.

The regulatory backdrop: Onchain, not CFTC regulated

This is also a good place to note that Opinion operates entirely outside the U.S. regulatory framework that governs its two largest competitors.

Kalshi has been the top fully CFTC-regulated designated contract market (DCM) in terms of prediction market volume, with KYC requirements, segregated customer accounts, and federal oversight. Polymarket acquired CFTC-licensed exchange QCX in July 2025 and began rolling out to US customers in December. Both platforms operate under the Commodity Exchange Act, which subjects them to market integrity rules designed to prevent wash trading, spoofing, and market manipulation.

Opinion operates on none of those rails. It’s a decentralized, no-KYC platform on BNB Chain, incorporated through a Hong Kong-based entity, settling trades in stablecoins. This is similar to how Polymarket’s main global platform operates, only it does so on the Polygon blockchain.

At Opinion, users connect a crypto wallet and trade permissionlessly. There are no segregated accounts, no federal oversight, and no registration with U.S. regulators. It geoblocks U.S. IP addresses, but enforcement is limited to the honor system and VPN detection. More than a dozen additional countries and territories are listed on Opinion’s restricted jurisdictions list, including China and the United Kingdom. Interestingly, the site also has a special pop-up notice against using its platform in Pennsylvania.

The onchain distinction doesn’t necessarily make Opinion illegitimate — plenty of successful crypto platforms operate outside U.S. jurisdiction. But it does mean the volume figures we’re about to examine aren’t subject to the same integrity safeguards that apply to Kalshi’s CFTC-reported data, which matters when you’re trying to compare platforms on equal footing.