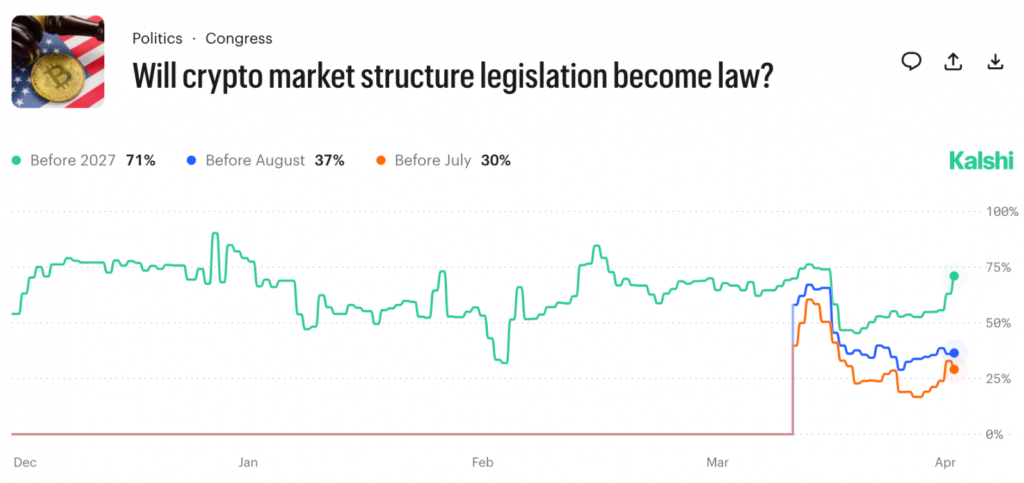

A new report from the White House Council of Economic Advisers (CEA) just rocked prediction markets on crypto legislation. On Kalshi, odds of US crypto market structure legislation passing before 2027 have been volatile, and they jumped roughly 15% following the release, from 55% to around 70%.

The CEA report landed with a surprising conclusion regarding the ongoing yield debate around Clarity Act legislation, and it heavily favors the crypto camp:

“A yield prohibition would do very little to protect bank lending, while forgoing the consumer benefits of competitive returns on stablecoin holdings.”

Running the numbers

According to the CEA’s findings, eliminating yield on stablecoins, the provision that banks have been pushing for, would increase bank lending by about $2.1 billion. That may sound like a lot, until you zoom out. Once put into perspective, it represents only around 0.02% of total lending, a fairly minimal impact for banks.

Even more striking is the finding that the policy would come with a significant cost to users. The report estimates “a net welfare cost of $800 million,” meaning $800M in lost value for users resulting in not having access to earning yield on stablecoin holdings.

The figure may have huge implications on the CLARITY Act, which has been stalled for months by exactly this fight.

What does this mean for the banks vs crypto debate?

These projections cut right into one of the biggest arguments banks have been making. Their idea has been that crypto exchanges offering stablecoin yield would result in “deposit flight” from banks, thus reducing banks’ lending capacity. That very concern has been a major driver behind stalled legislation.

But the report suggests that this very effect is being overstated by a wide margin, and may in fact be completely insignificant.

That raises a bigger question about whether the proposed policy is even solving the problem it’s meant to address.

Why is the impact so small?

The reason the impact is so small on bank lending simply comes down to how money actually flows through the system. When someone moves money into a stablecoin, it’s not disappearing from banking. It’s just being recycled.

The stablecoin issuer takes those dollars and buys safe assets like Treasury bills. The seller of those assets then deposits the cash back into a bank. So while one bank may lose a deposit, another bank gains one.

At the system level, the money is still sitting in a bank. Those dollars aren’t going anywhere; the deposits are just shifting around.

So what are banks actually competing on?

If lending isn’t genuinely at risk, then the real competition isn’t about deposits. What really changes is who sits between the user and the money in the system.

Stablecoins push the experience into wallets and apps, turning banks into background infrastructure. That means banks risk losing payments, fees, and control over the customer relationship.

Yield matters not because it drains deposits, but because it turns stablecoins into something people hold, not just use. It pulls users into crypto platforms and keeps them there. If you take yield away, then stablecoins become less “sticky.” So the real competition isn’t for the dollars, but rather for the interface, the fees, and the customers.

Stablecoins could be good for small banks

While larger banks voice their concern for potential losses, other industry figures are considering the benefits of stablecoins for smaller banks.

Coinbase Chief Policy Officer, Faryar Shirzad, explained in a post why “stablecoins are an opportunity and not a threat”:

Stablecoins make payments cheaper, faster and more accessible.

— Faryar Shirzad 🛡️ (@faryarshirzad) April 8, 2026

This is good for the American people, but also for banks, particularly small banks who will be able to offer a broader range of payment services without the infrastructure of big banks.

It's good to see the…

How does that work? Large banks already have powerful payment systems. They can move money globally, handle foreign exchange, and settle transactions quickly.

But smaller banks don’t have that same level of infrastructure. Instead, they usually rely on middlemen, which makes transfers slower and more expensive.

If stablecoins aren’t actually pulling money out of the banking system, then they’re not taking deposits away from those smaller banks. Instead, they can act more like shared infrastructure that any bank can use.

That gives smaller banks the opportunity to tap into faster and cheaper global payments, without building it out themselves, giving them a better shot at competing on services.

The yield loophole and what happens if it’s closed

It’s worth noting that stablecoin yield hasn’t actually disappeared, at least not just yet. The GENIUS Act blocks issuers from paying it directly, but platforms can still offer rewards through revenue-sharing, so users can still earn something on their stablecoin activity.

On the other hand, some versions of the CLARITY Act aim to close that gap completely. If that happens, stablecoins likely become less attractive to hold, but the demand for yield won’t just go away. Instead, it shifts into DeFi, offshore platforms, or new workarounds, while bank lending still barely moves.

So the policy doesn’t really solve the original concern, but rather just changes where the activity happens. If that is the case, it would make sense to find a suitable middle ground if legislators’ priorities are indeed centered on investor safety and keeping digital finance thriving in the US.

What can we expect going forward?

The White House’s CEA report may just tip the scales in favor of crypto for progress with the CLARITY act, with recent prediction market activity supporting that notion. If stablecoins aren’t actually hurting bank lending, then the banking industry’s main reason for banning yield falls apart.

Naturally, the focus may now move away from the “hazards” of stablecoins, and more so toward how much they should be allowed to compete. Banks will still push for tighter rules, but it will now be much harder for them to argue for an outright ban on yield using the lending argument alone.

A more likely outcome is somewhere in the middle. Limits on passive yield, but some room for rewards tied to how people actually use stablecoins. In practice, that means stablecoins probably aren’t completely shut down or fully opened up, but they’ll be folded into the system.

And the real question becomes: What role will they be allowed to play?