Uncategorized

Polymarket Traders Knew The Weeknd Was Going to Beat Drake on Spotify Wrapped

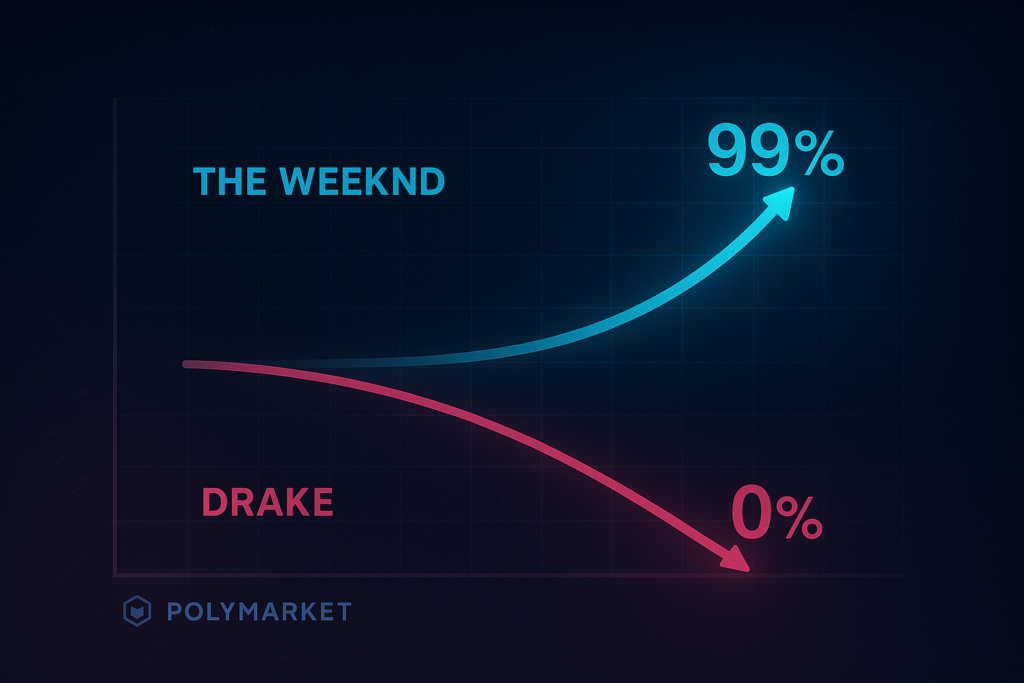

Hours before Spotify announced its 2025 Wrapped results, the odds on The Weeknd finishing third on Polymarket’s contract surged from 40% to 99%. Polymarket shared the news on X, framing...

Cheryle Shepstone

December 4, 2025